SaaSletter - April 2024 SaaS Demand Index

Plus Our Employment Index + Cloud Cost Optimization Data

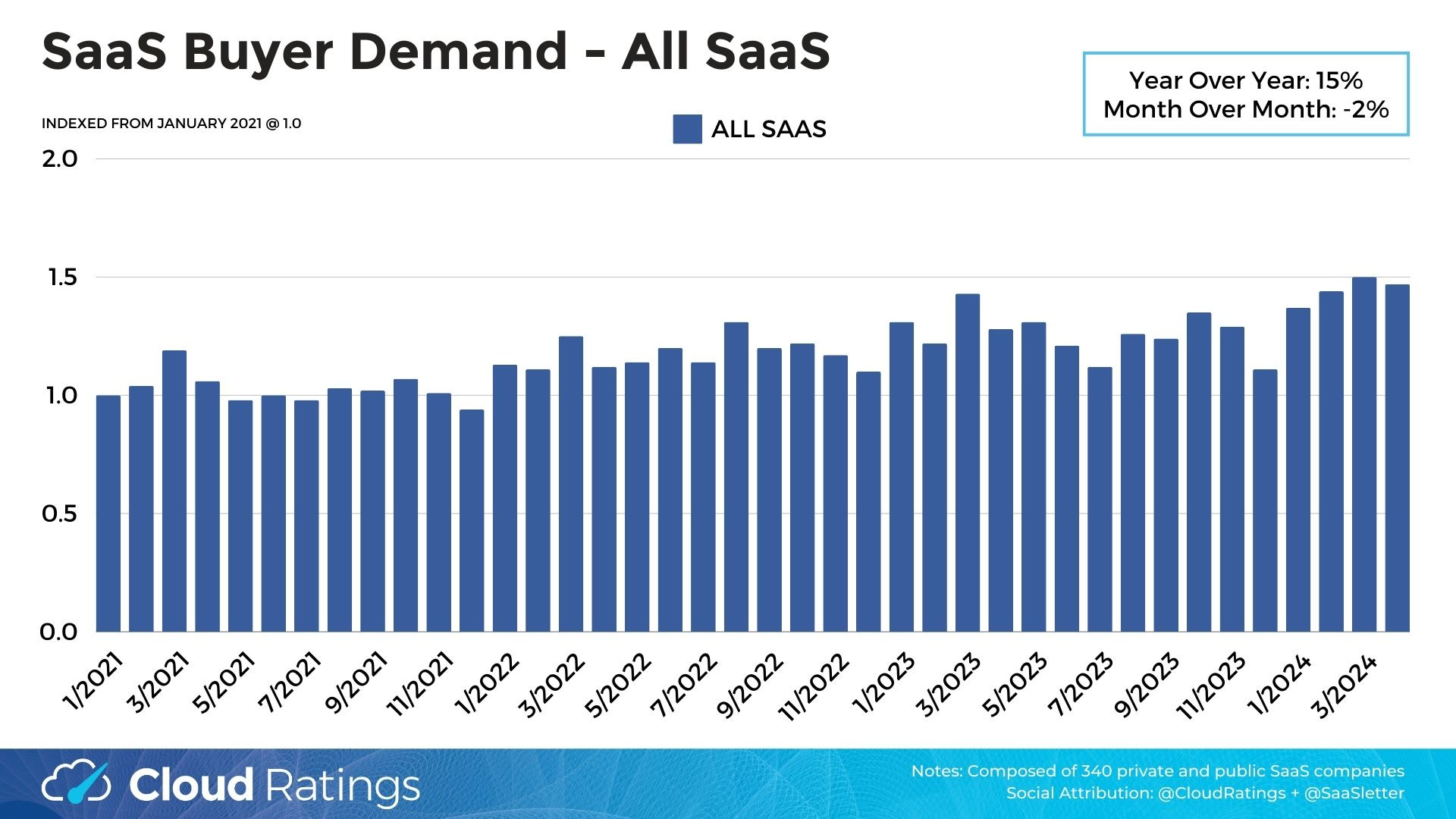

April Demand Index

We’re excited to update the SaaS Demand Index with data through April 2024.

For our new readers: the Demand Index is derived from high-intent (aka “okta pricing”) Google Search volume data for 340 companies, covering 350,000+ searches each month.

Reminder: this is a directional, free, and ever-evolving* analysis → always do your own due diligence.

Moreover, the data captured here is best characterized as top-of-funnel or dark funnel → factoring in sales cycle length, do NOT use this Demand Index as a predictor of near-term financial results and/or financial guidance.

Industry-Wide Data

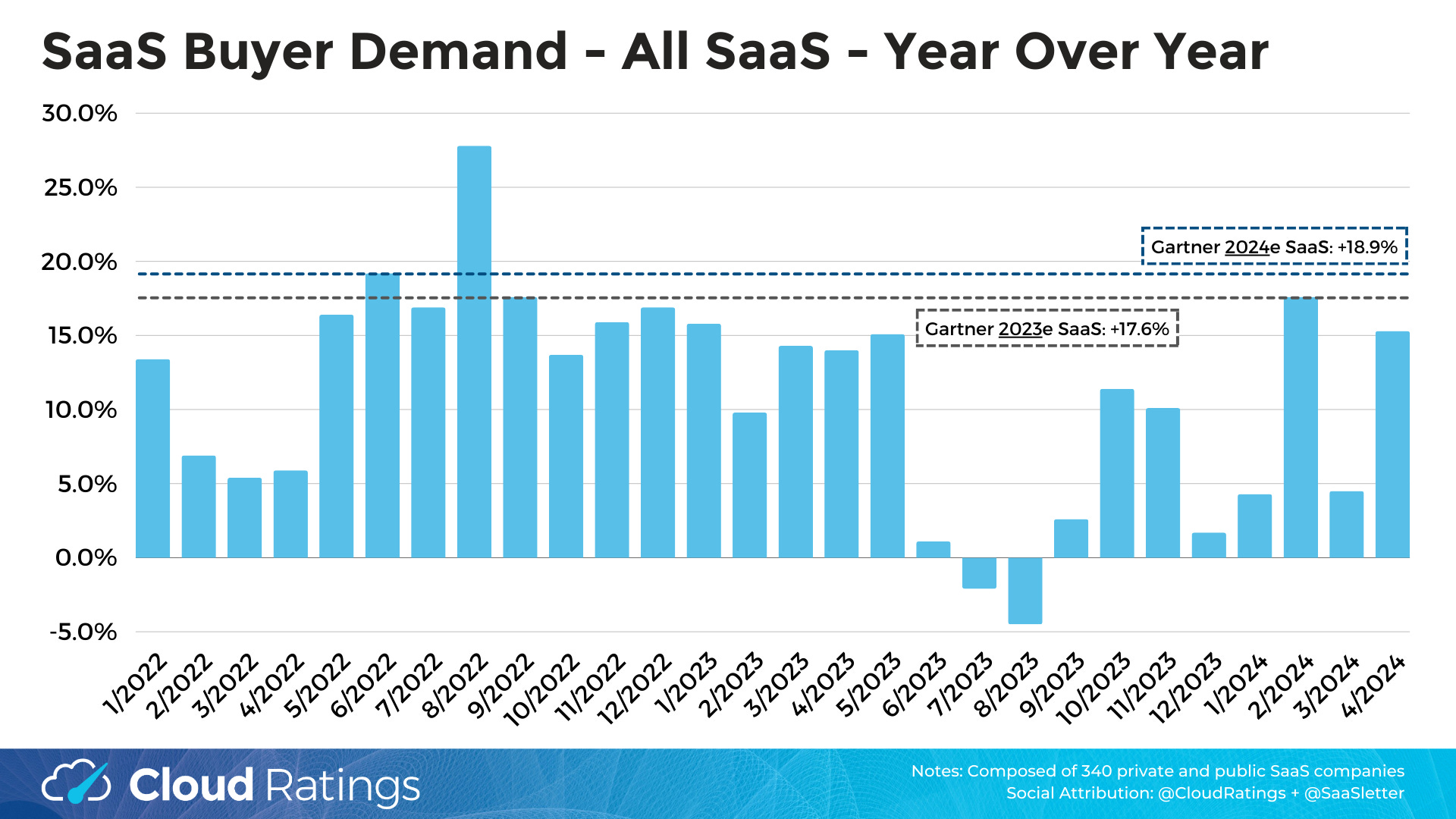

High-intent search volumes were down -2% month-over-month and +15% year-over-year.

When combined with February 2024’s +18% YoY reading, April’s +15% *possibly* marks a shift from the doldrums period of June 2023 to January 2024.

The new YoY graph above compares the high-intent search trends to Gartner’s 2024 cloud spending forecast only to give context. We note possible “apples versus oranges” dynamics when comparing the SaaS Demand Index versus Gartner:

potential buying journey shifts away from Google search and now starting on review platforms (like G2) and - to a lesser extent in terms of measurable impact - community recommendations (like private executive Slack groups).

a general trend for Google search volumes to plateau with scale. We’ve also observed this dynamic with retailers.

most importantly, the SaaS Demand Index is a *forward indicator*, whereas Gartner’s market sizing and growth capture *realized revenue* → given sales cycles, “lagging” our SaaS Demand Index is the right way to examine correlation.

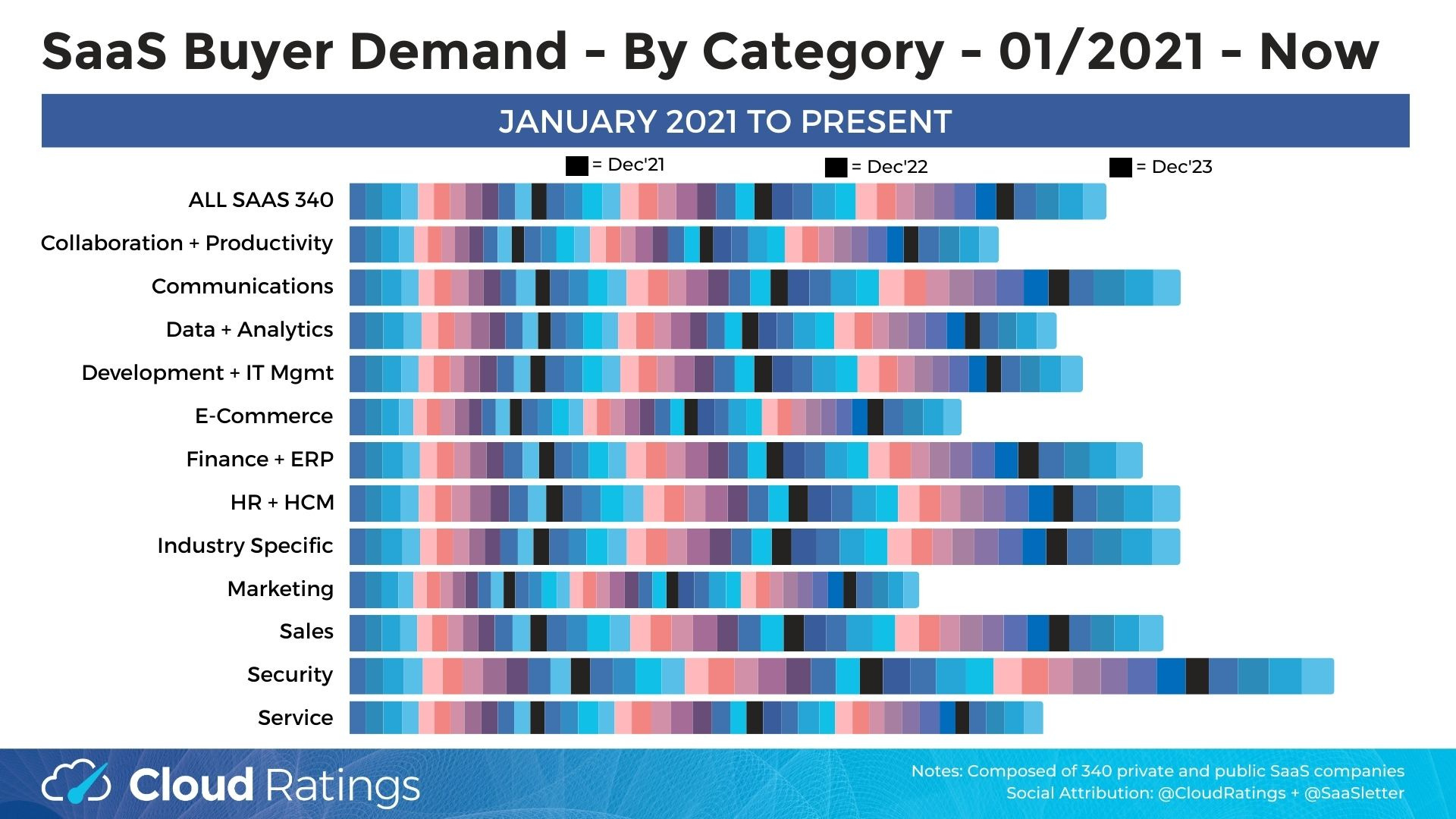

Trends By Product Category

Zooming out to recap almost three years of data on our cumulative growth since January 2021 slide:

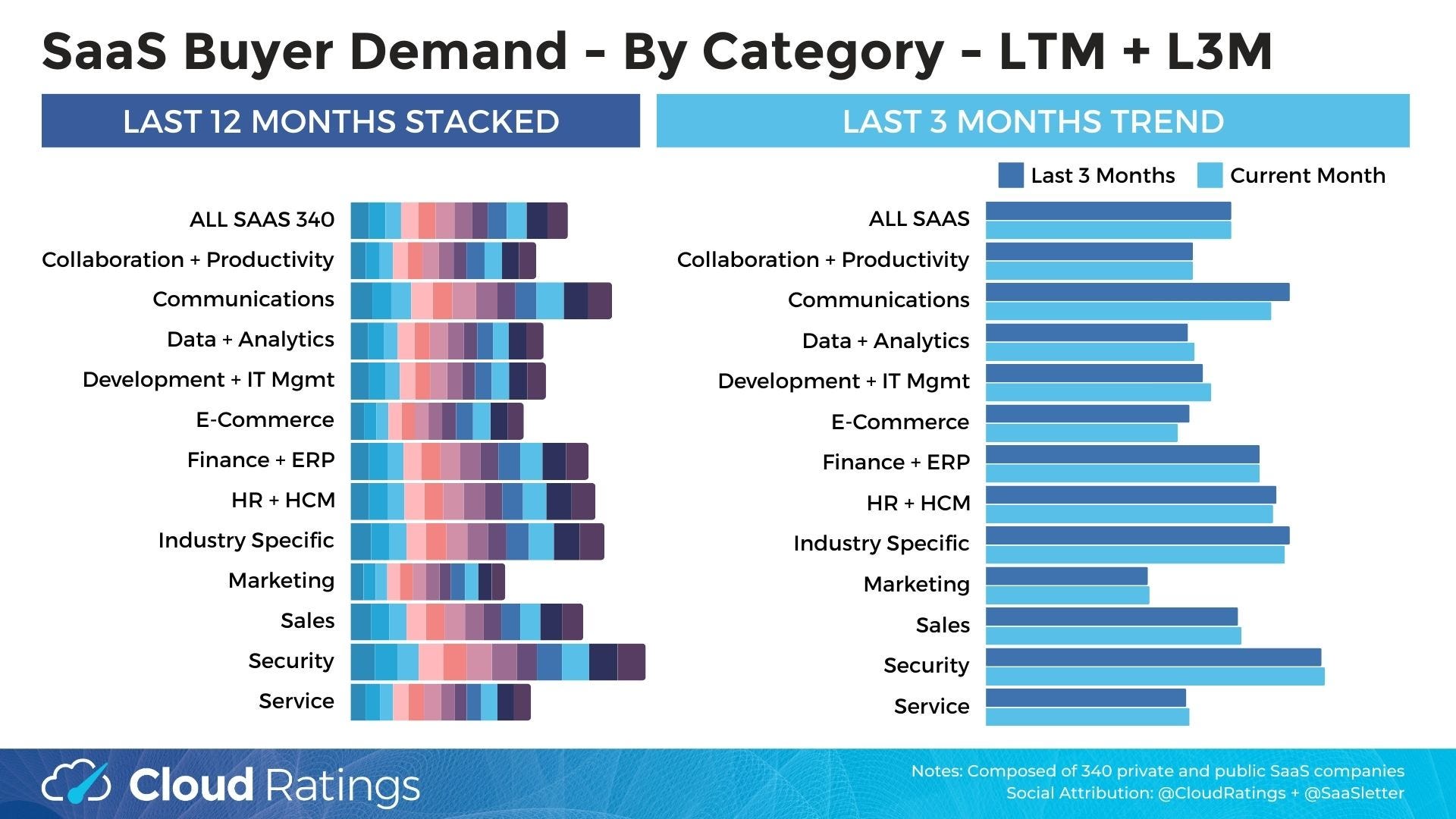

This slide presents growth for the last month and last three months, respectively:

Callouts from recent trends:

Above Average Performers: Consistent with prior months, the strong performers were Security, Communications (likely attributable to MessageBird’s price cut), Industry Specific / Vertical, HR + HCM, and Finance + ERP.

Top Performing Companies - Past 3 Months (with publicly-traded in bold): Microsoft Dynamics, Paylocity, Jobber, Guidewire, Veeva, FloQast, Shopmonkey, Wiz, Dayforce, Gladly, VMware, Tenable, Genesys, Chorus, Retool, Homebase, Collibra, RevenueCat, ServiceMax, SmartRecruiters, Guru, Workable, BlackLine, Braze, Calabrio, Celonis, Rainforest QA, RealPage, SailPoint, Yardi, OneTrust, MyCase, CrowdStrike, Loopio, Clari, Klaviyo

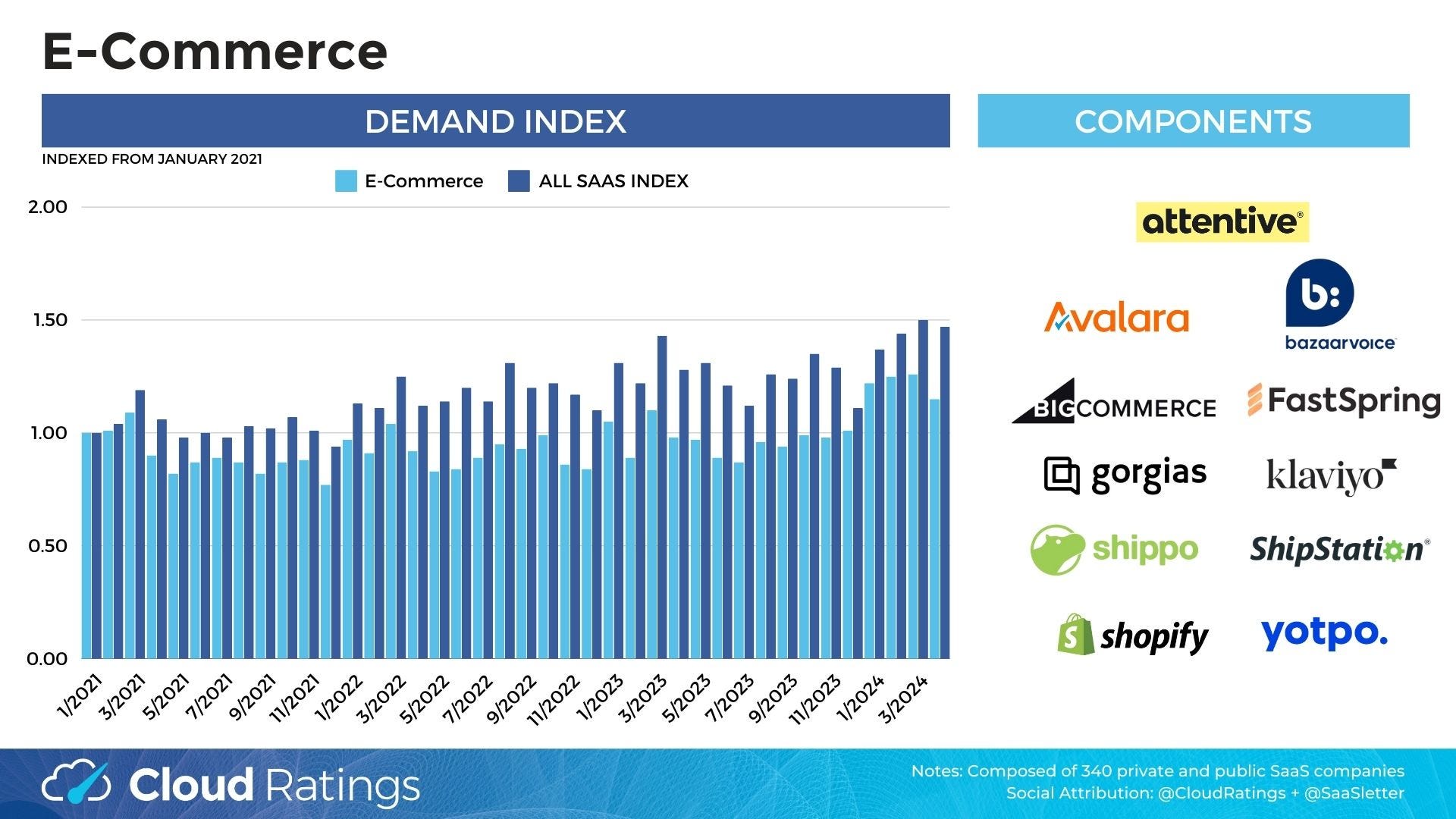

All of the category drill-downs - like this E-commerce example - are available in this slide PDF:

Other Trends

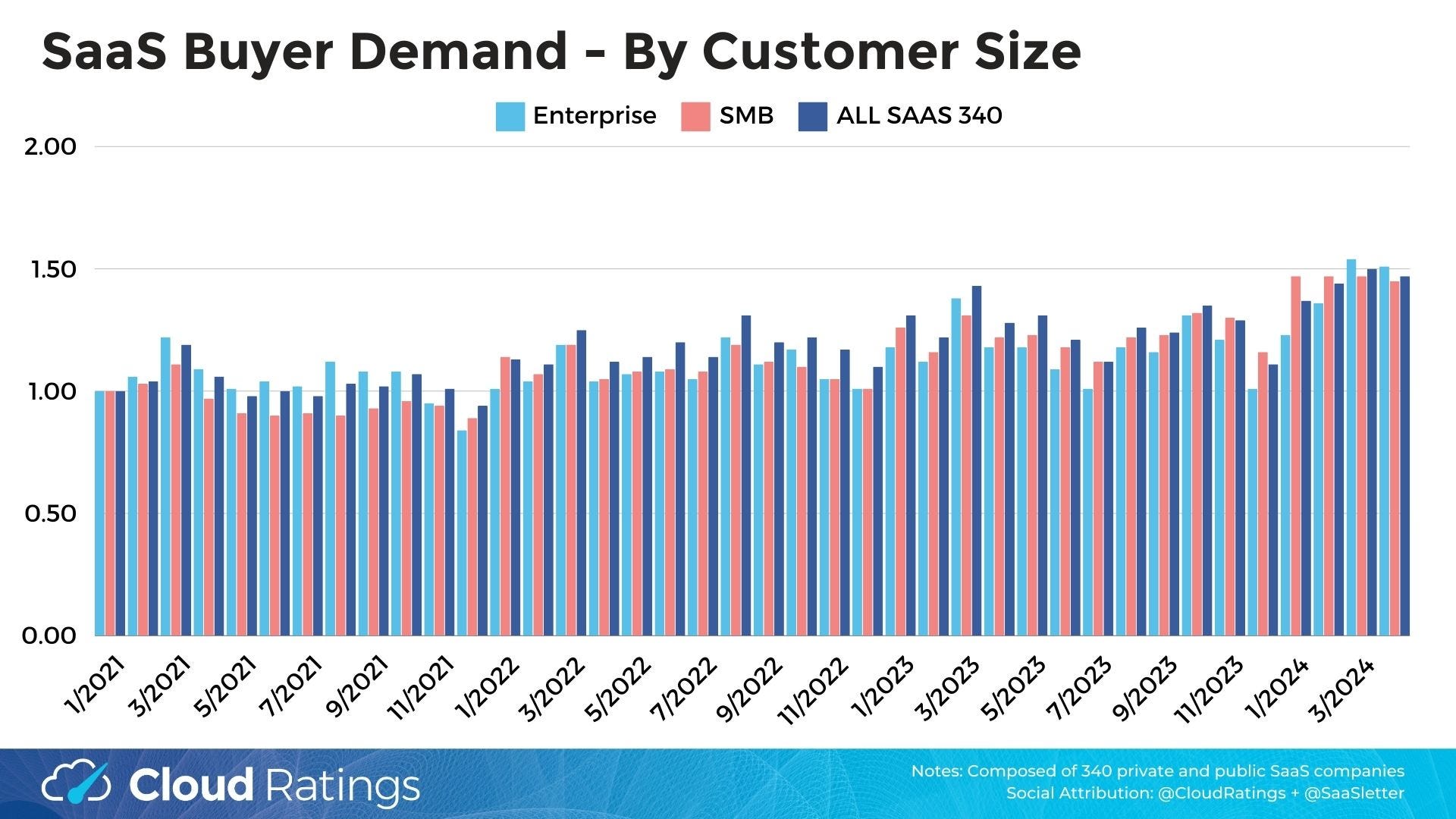

By customer mix, Enterprise again outperformed SMB in April, reversing a recent trend of SMB > Enterprise:

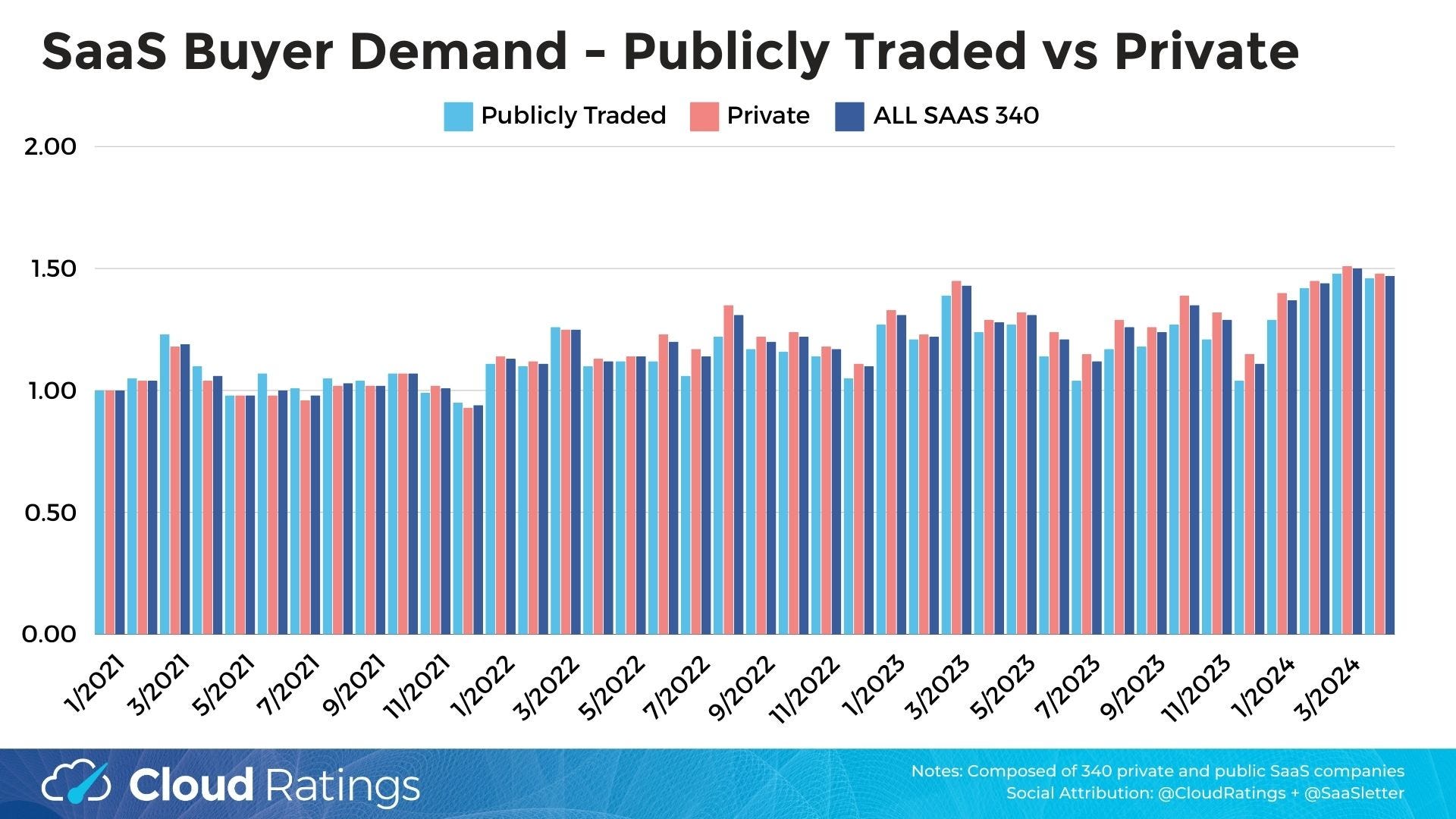

The gap between private companies and publicly traded SaaS has narrowed of late:

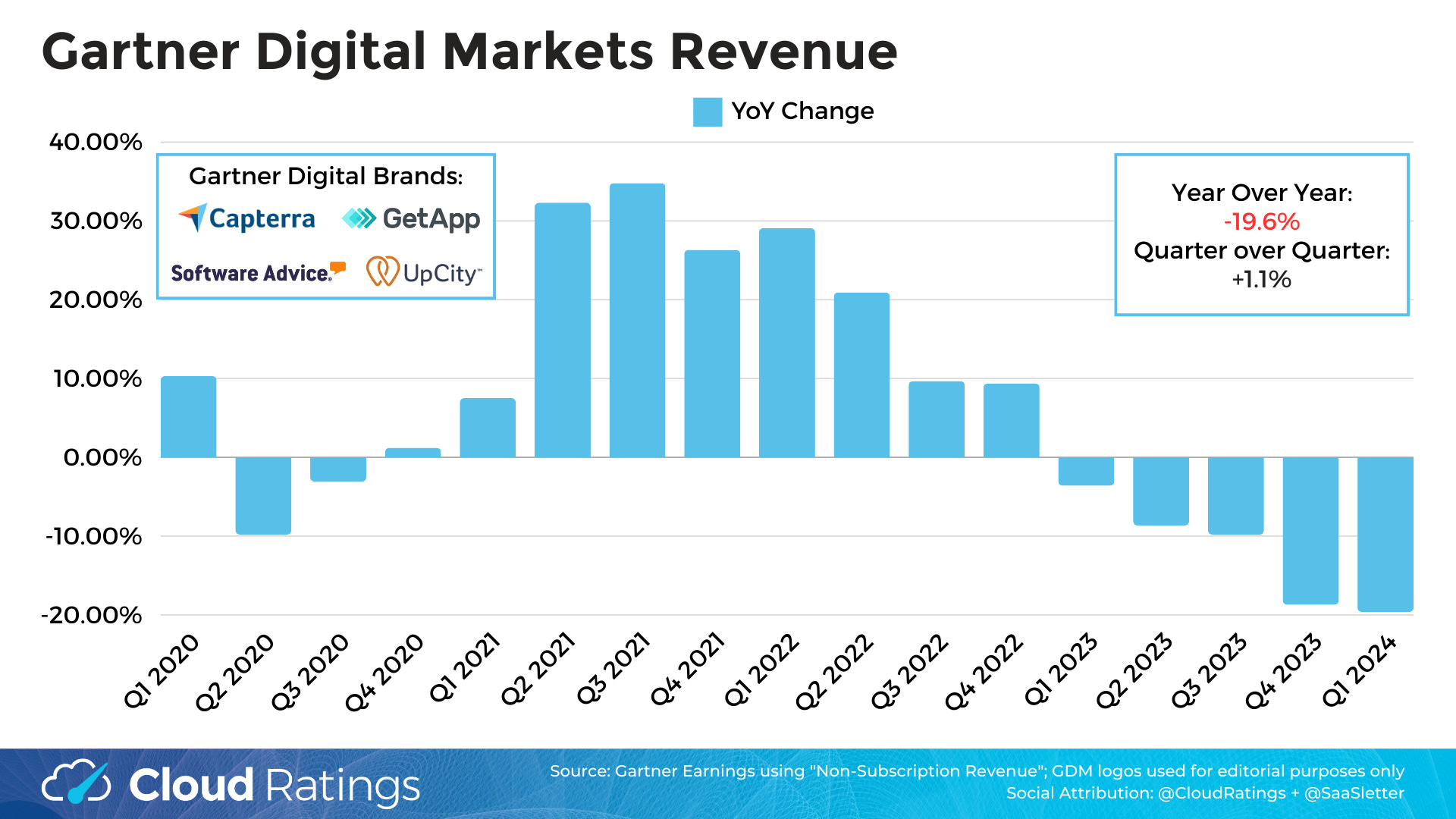

We also track Gartner Digital Markets revenue trends quarterly. Why? Since it captures both *buyer interest* (traffic on sites like Capterra) and software *vendor marketing spend* (their cost-per-click bids + budgets on Capterra).

Q1 2024 revenue trends were weak:

April SaaS Employment Index

As a reminder, our SaaS Employment Index covers employment trends for 3,500+ private US HQ’ed software companies. Slides for this month are available here:

The key points:

Strong hiring below 200 FTEs; 200+ = weak but improving

Engineering continues to be weak (versus Marketing and Sales functions) - an AI CoPilot impact?

Notably, strong sales hiring amongst private equity-backed companies

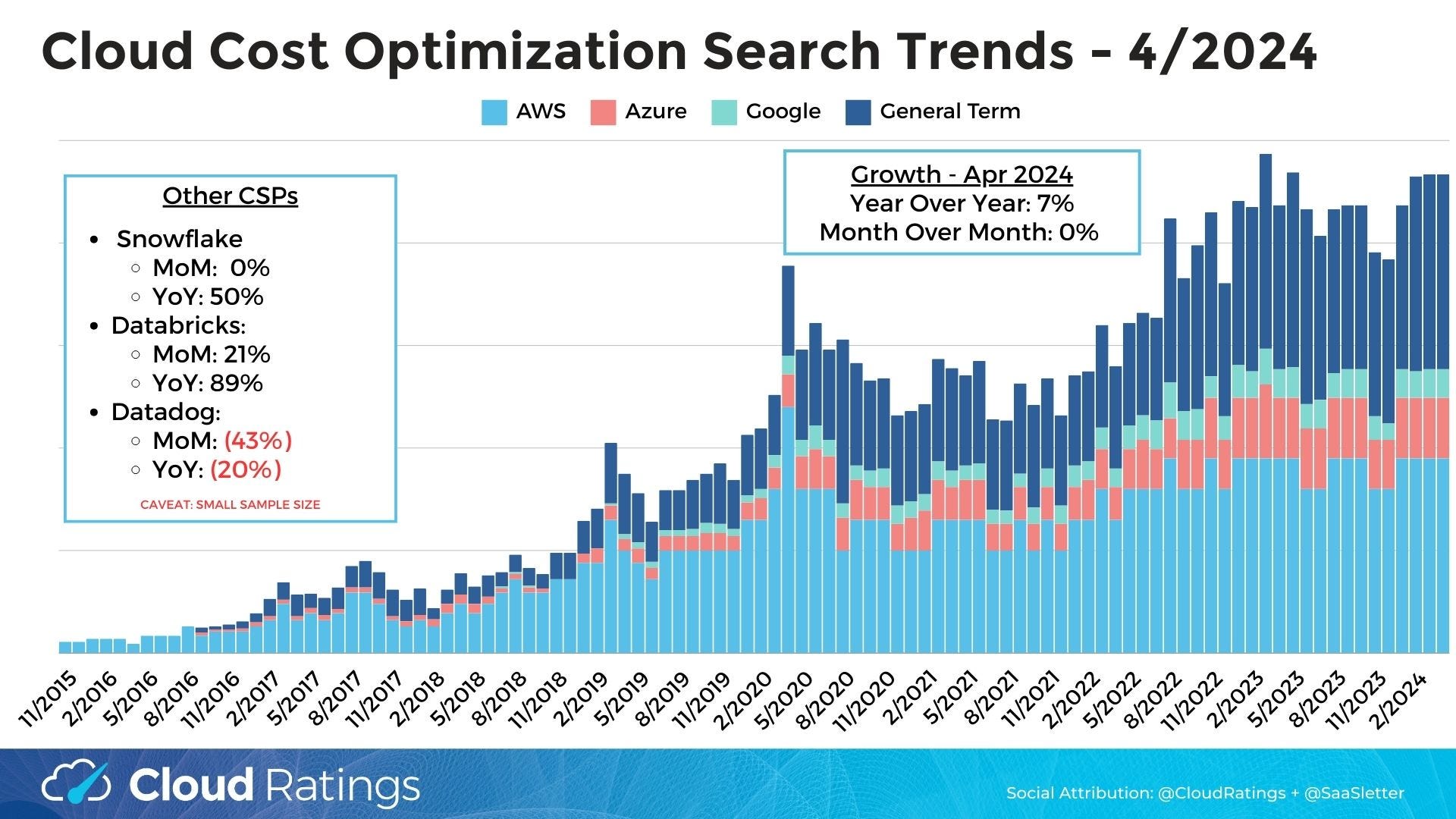

Cloud Cost Optimization Trend Update

The general plateau trend continued in April: cost containment searches were up 7% year over year and flat at 0% month over month.

Notably (though not on the graph), April was the seventh straight month that Snowflake exceeded Google Cloud in absolute search volume.

*To publish closest to month end, we are accessing the underlying API data “early” (relative to the typical SEO and PPC users that do not require such immediacy). Therefore data should be considered “provisional” (i.e. subject to revision by our data provider) and create volatility in the data presented in the 2 most recent months.

This report was first published on cloudratings.com.