SaaSletter - Can Superior NRR Offset Weak AI Gross Margins?

Plus A Deep Dive Into Fullcast's 2026 GTM Benchmarks

Before exploring the efficient frontier of AI NRR vs gross margins, a deep dive into Fullcast x Pavilion 2026 GTM Benchmarks:

Fullcast 2026 GTM Benchmarks

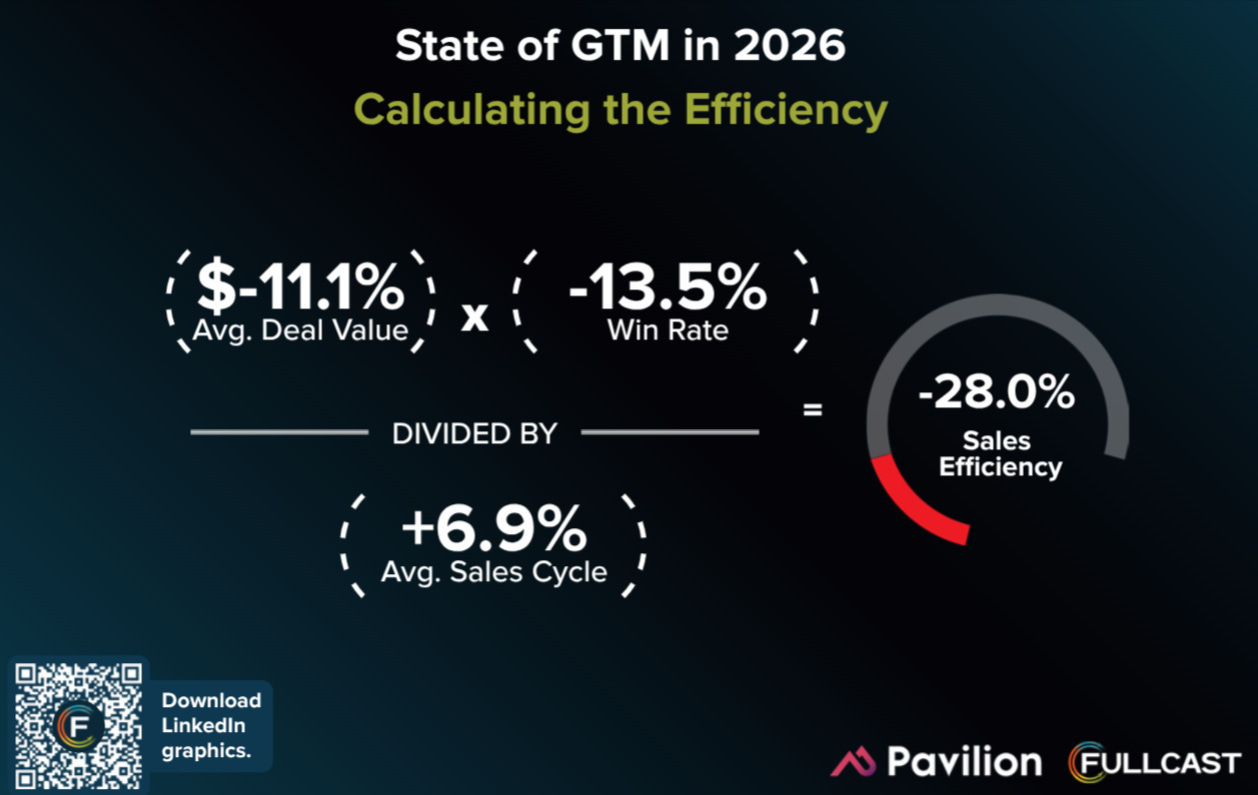

While last week we covered ICONIQ’s “2026 State of GTM“ positive trends in areas like win rates and sales cycles, the latest GTM benchmarks from Fullcast paint a more sobering picture.

We’ve covered the Fullcast (formerly Ebsta pre-acquisition by Fullcast) / Pavilion benchmarks each edition for years now due to a) granularity and b) sample size (this year = $78 billion of sales opportunities). Key highlights:

Sales efficiency and win rates continue to be poor, in absolute and directional terms:

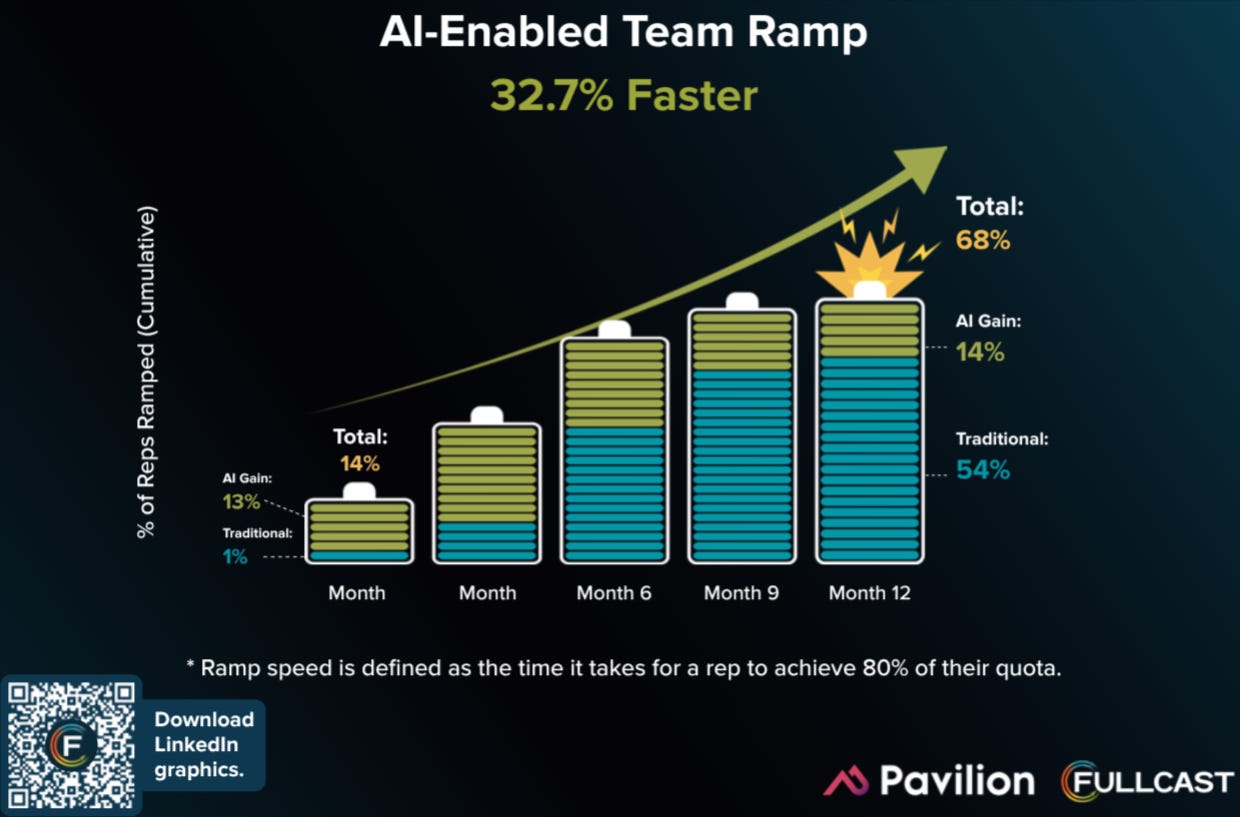

AI is accelerating seller ramps:

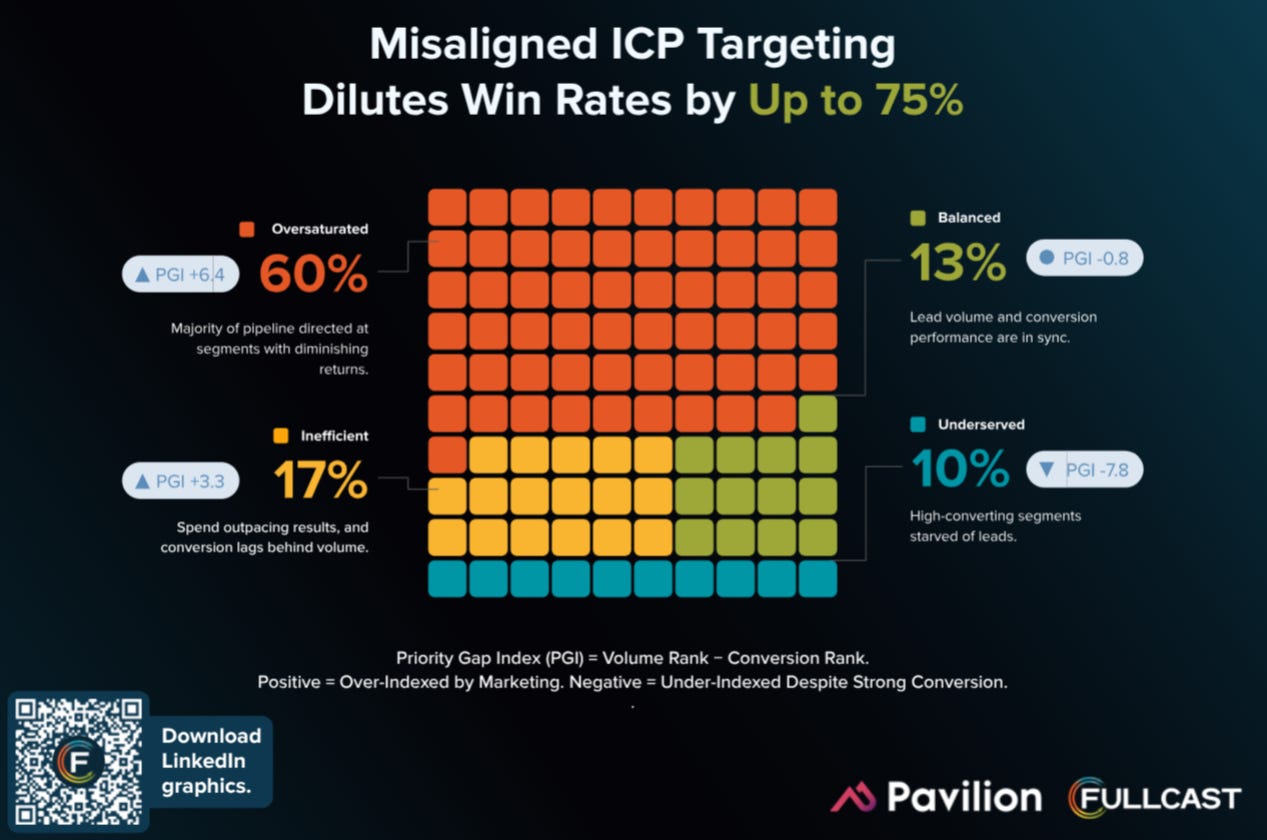

Poor pipeline ICP mix very likely contributes to poor absolute win rate levels

Tactical call out - outbound BDR efforts 80% below average efficiency → in a noisy AI world, is this SDR cold outreach playbook dead + a brand net negative?

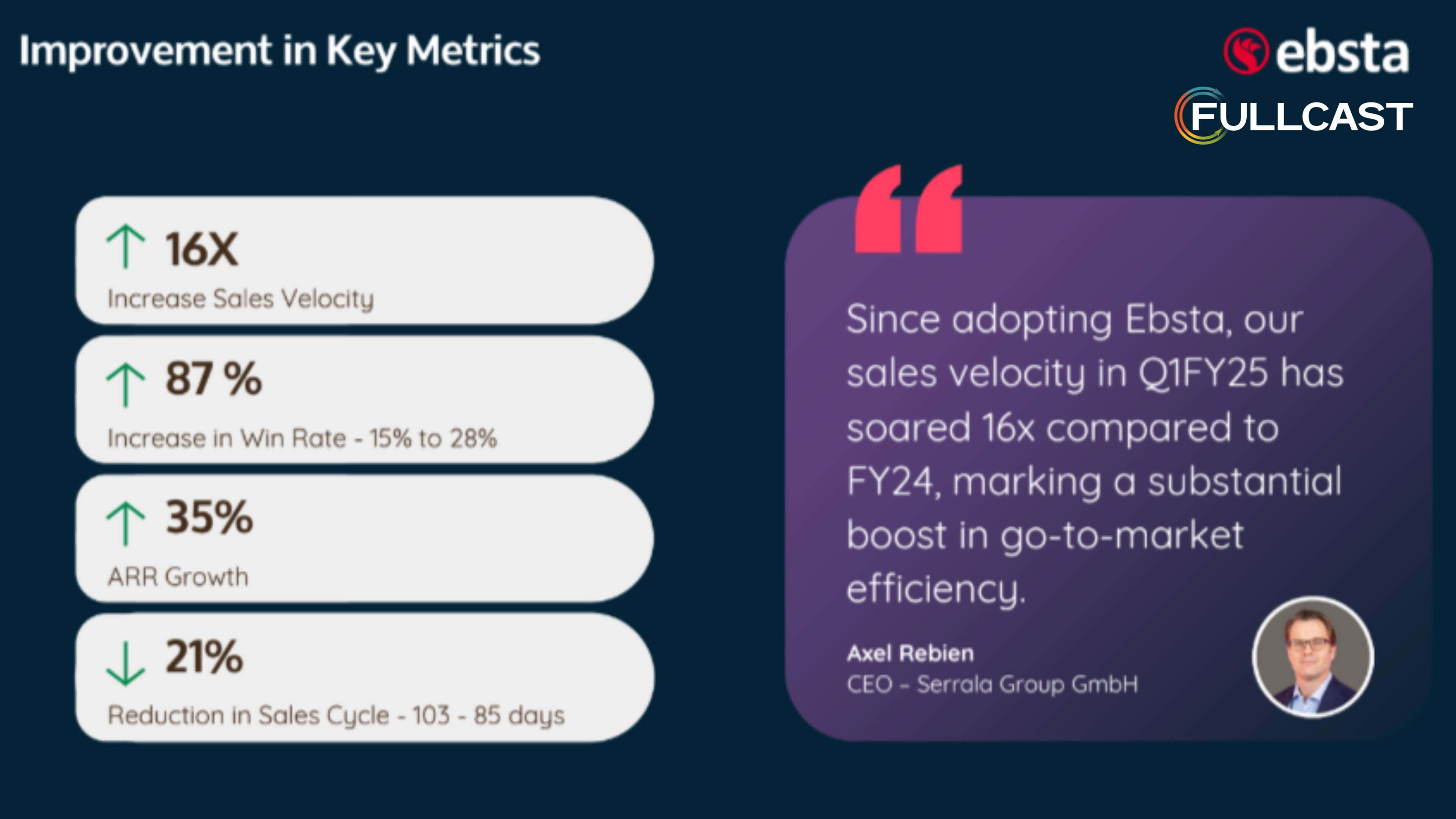

Fullcast Revenue Insights As A Service

We are helping Fullcast + Guy Rubin connect with software private equity investment firms to grow their Revenue Insights as a Service (RIaaS) offering:

quarterly deep dives into your portco’s sales machine,

using a mix of AI/software (linked into CRMs, email, and call recordings)

with a professional services element that yields this type of report (attached)

Full Fullcast RIaaS overview deck here + book a demo

Can Superior NRR Offset Weak AI Gross Margins?

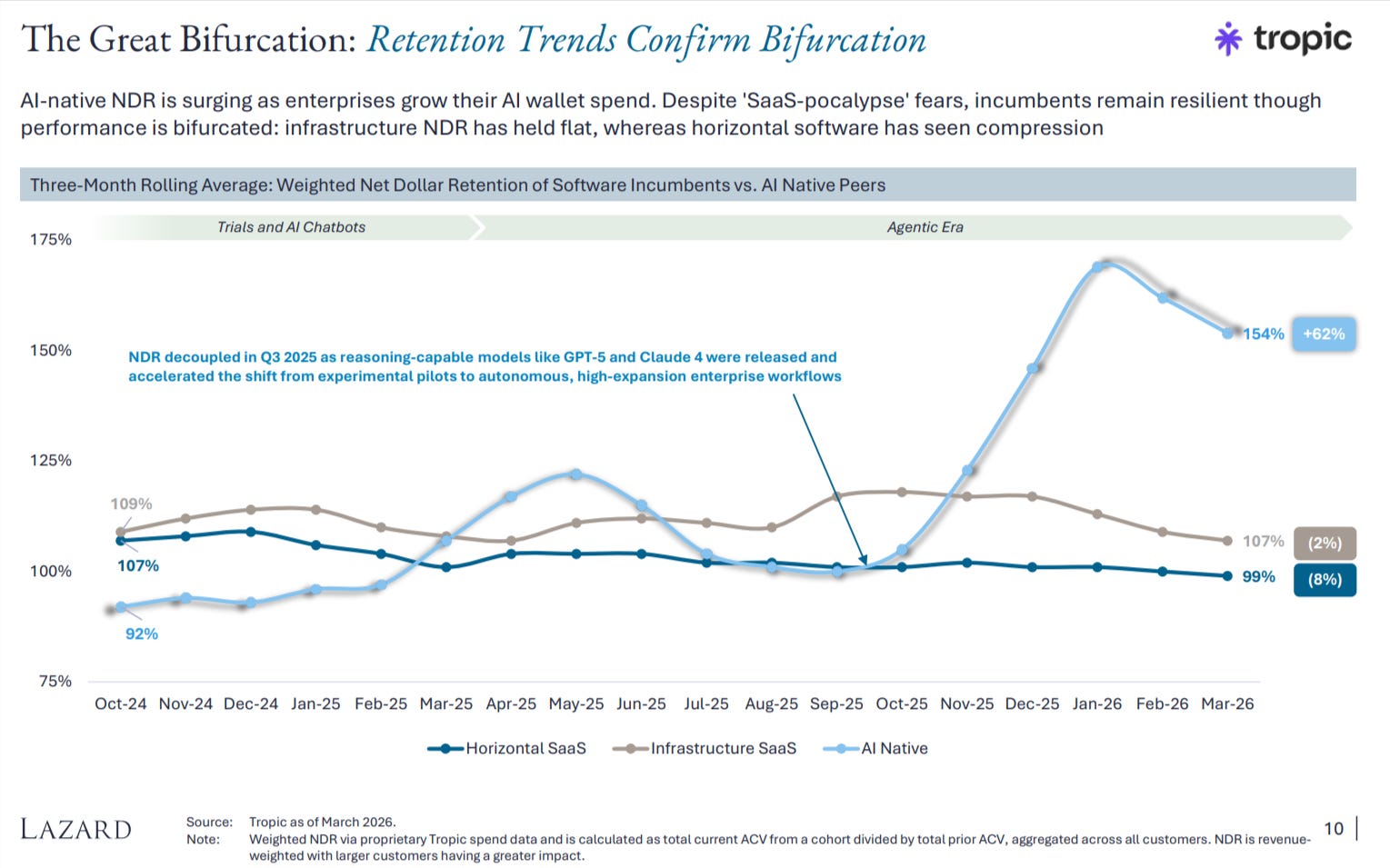

Inspired by this AI vs SaaS NRR data via Tropic (a software spend management platform covering ~$20 billion of spend) in Lazard’s “AI Impact on Technology M&A” deck (60 slides)…

The eye-popping AI NRR of 154% inspired a theoretical cross-check: Can Superior NRR Offset Weak AI Gross Margins?

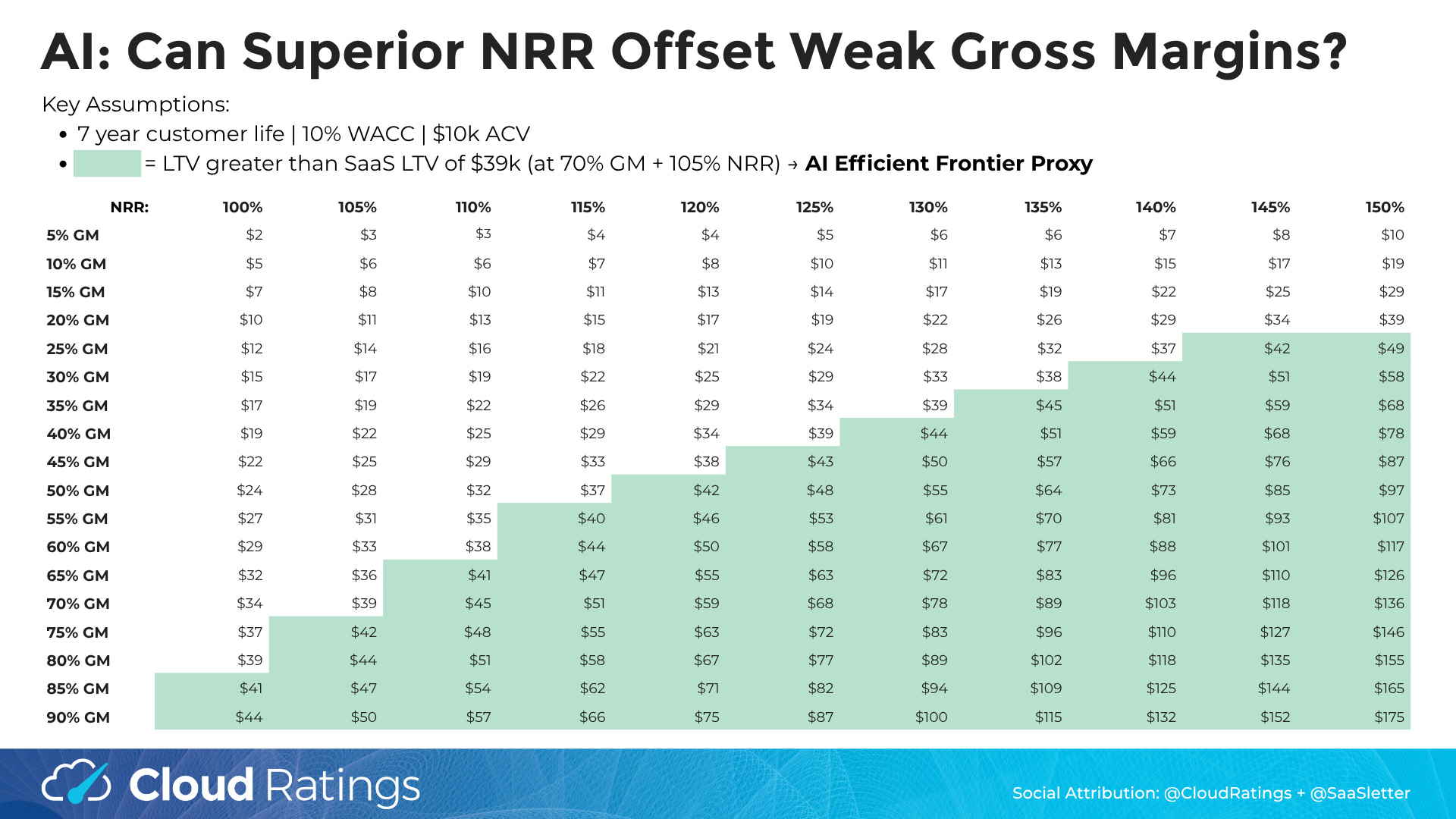

The key assumptions and rationale: SaaS unit economics are well-established, with a reasonable baseline of roughly 105% net revenue retention (NRR) and 70% gross margin.

We applied a 7-year expected customer life (84% gross retention, so below core Mid-Market / Enterprise GRR levels… while recognizing 7 years is an eternity in terms of technical disruption) and a 10% discount rate.

Under these assumptions, a $10k ACV SaaS customer has an NPV of $39k.

This NRR vs Gross Margin sensitivity table helps frame the “efficient frontier” for AI apps:

Translating a bit, AI apps can have SaaS customer unit economics at these thresholds:

At 50% AI gross margin, need NRR of ~118%

At 40% AI gross margin, need NRR of ~130%

At 30% AI gross margin, need NRR of ~141%

At 30% AI gross margin, need NRR of ~150%

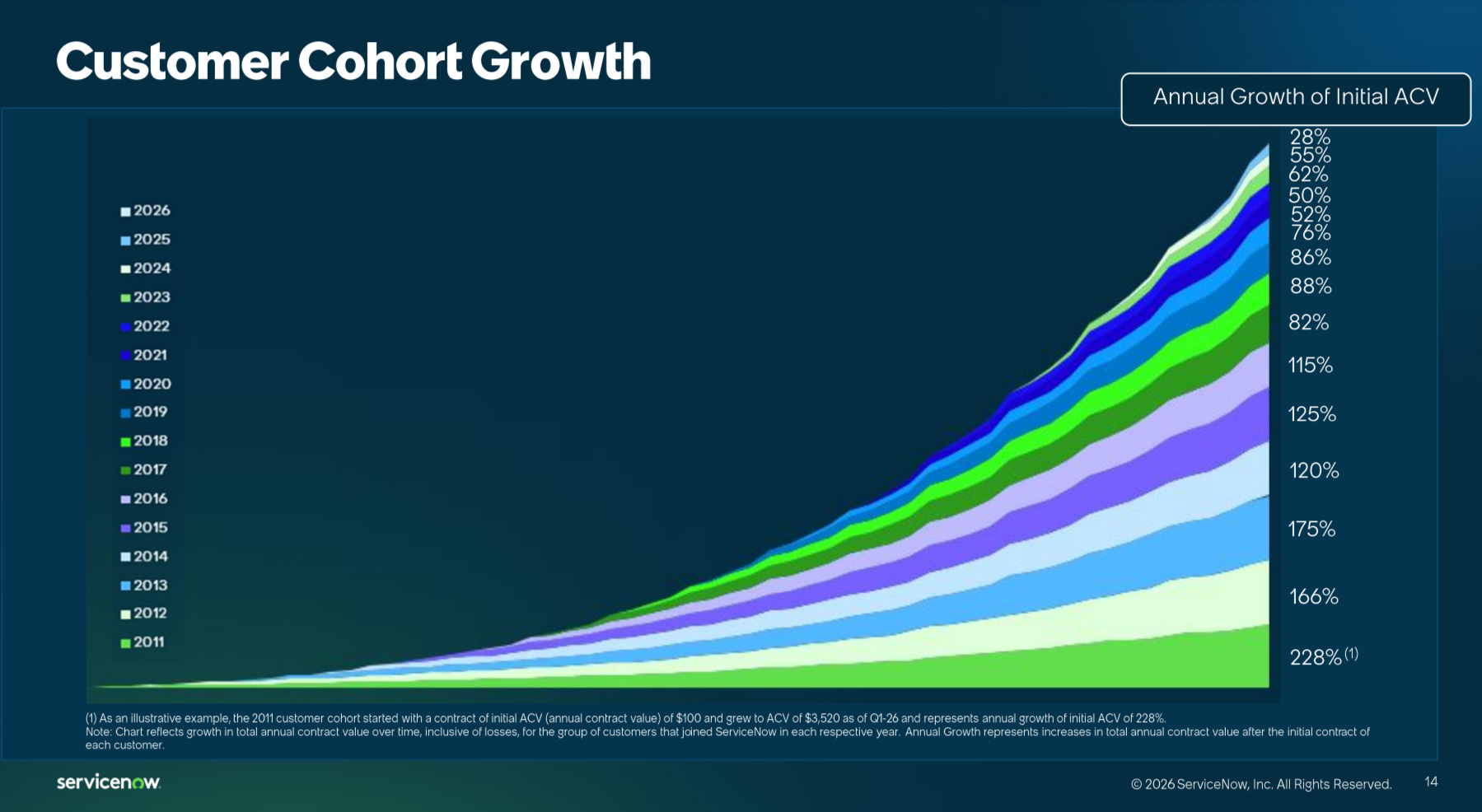

Of course, 130%-%150% NRRs over 7 years translate into exiting ACVs of $48k-$113k off of a $10k starting base! Meaning you would be underwriting towards ServiceNow’s legendary cohort growth (via latest ServiceNow Investor Presentation):

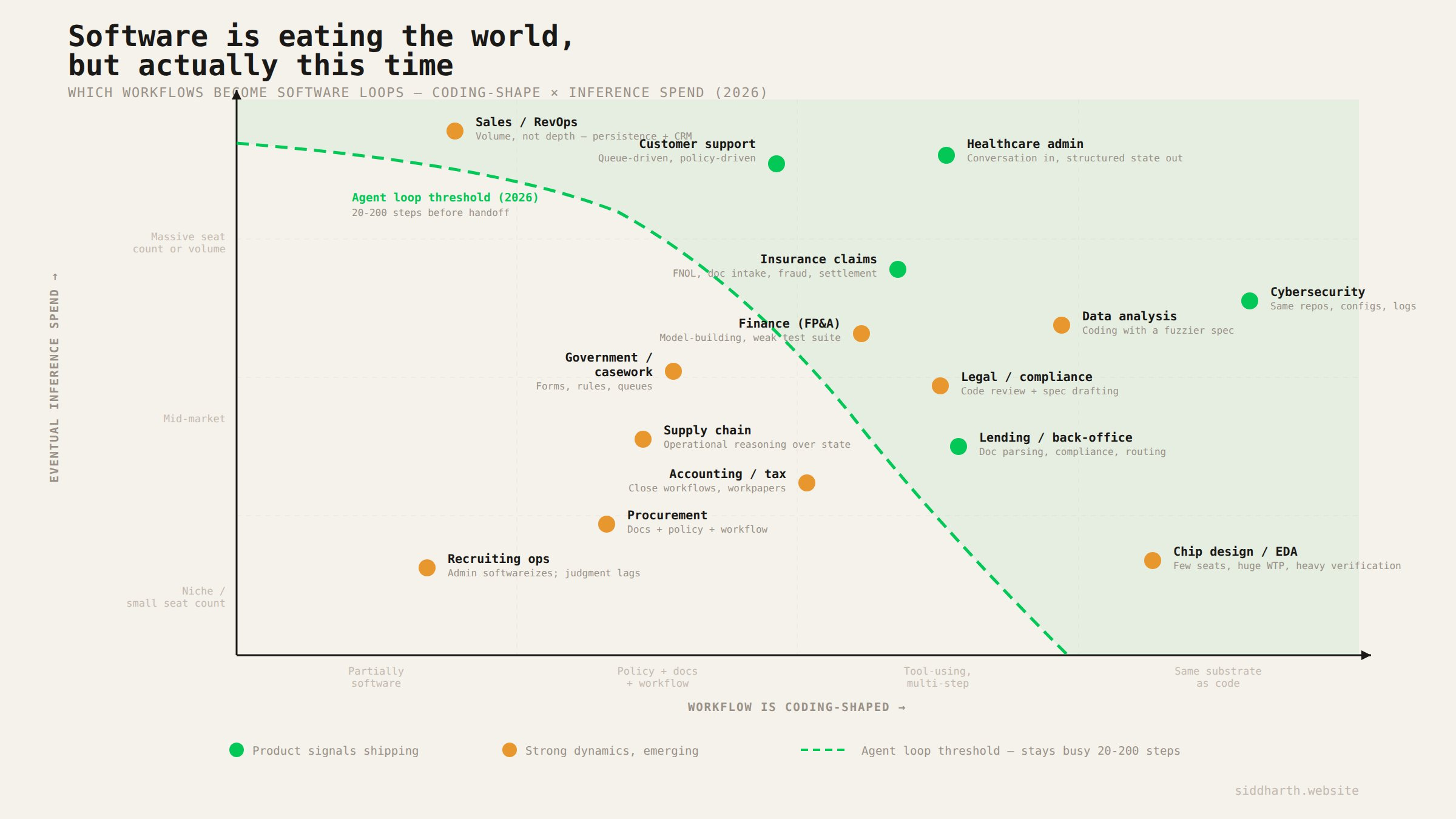

Inference Is Eating the World

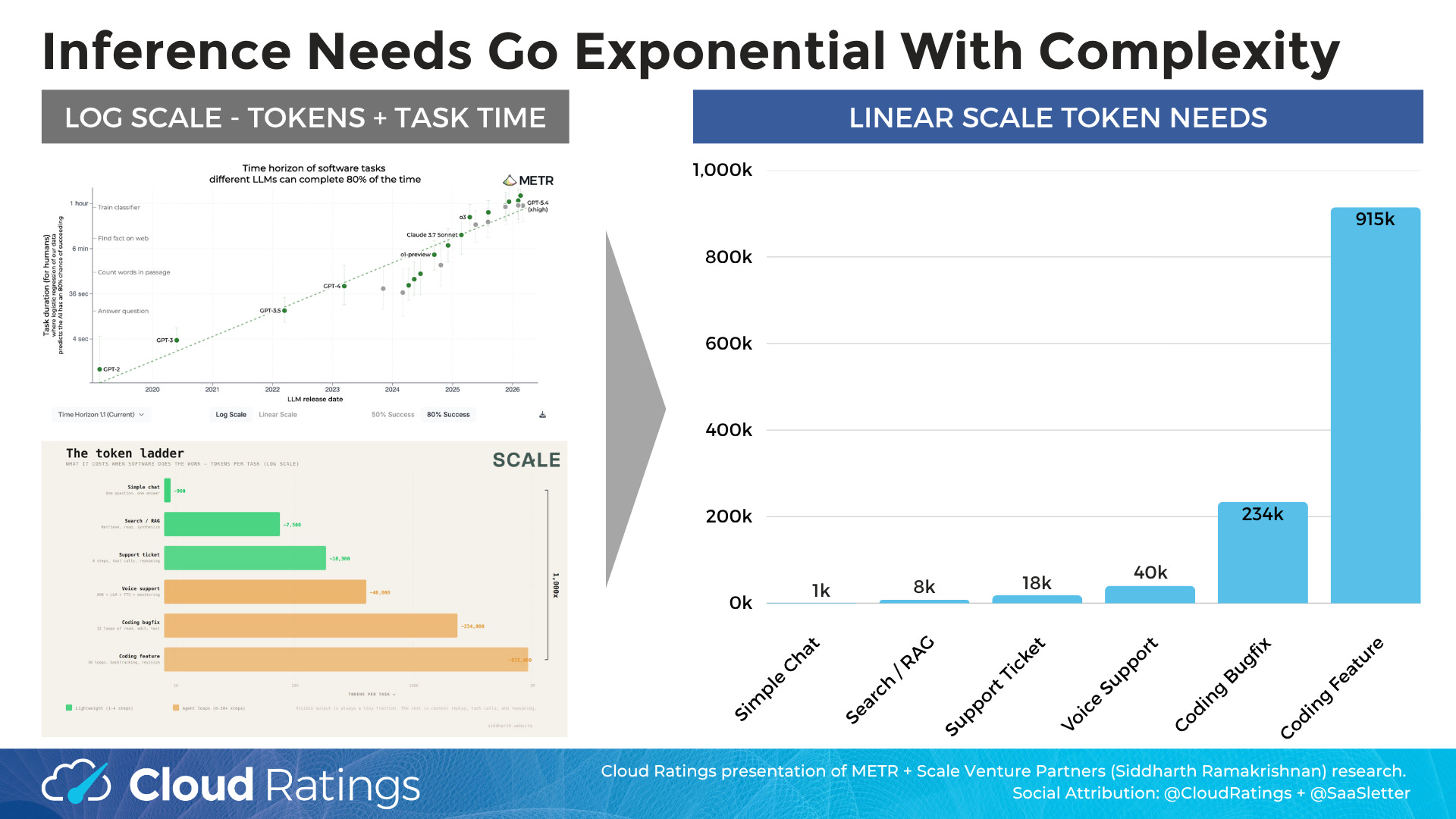

Siddharth Ramakrishnan of Scale Venture Partners (h/t Rory O’Driscoll) published a thoughtful “Software Is Eating the World (But Actually This Time)” where he does a good job outlining the less visible complexity and increasing inference needs in AI workflows (our emphasis = bold):

Take a voice support agent handling something simple but real, like rescheduling a medical appointment. To the customer, it feels like one conversation. Under the hood, it is a small autonomous system running continuously. As the caller speaks, a speech recognition model transcribes audio in real time. An orchestration model then reasons over the transcript, pulls the patient record, checks scheduling constraints, looks up provider availability, decides what to ask next, and calls the relevant tools. Once it has enough information, it synthesizes the result into a response, and a text-to-speech model turns that back into natural audio. In parallel, other models may be monitoring sentiment, checking compliance, or deciding whether the call should be escalated.

The system is doing all the work itself: listening, retrieving, deciding, tool-calling, verifying, and responding in a loop. An 8 minute call might contain only ~3k tokens of raw transcript, but the orchestration layer can easily consume ~40k tokens once you account for repeated reasoning over the growing conversation, retrieved context, and tool outputs, on top of continuous ASR and TTS inference running for the duration of the call. “One AI phone call” is really a multi-model inference stack operating continuously.

To help call out to the human eye what this means for token + inference needs, we translated the article charts from log to linear scale:

As always, go read the full post which includes deeper insights like:

Avenir on Anthropic vs Microsoft

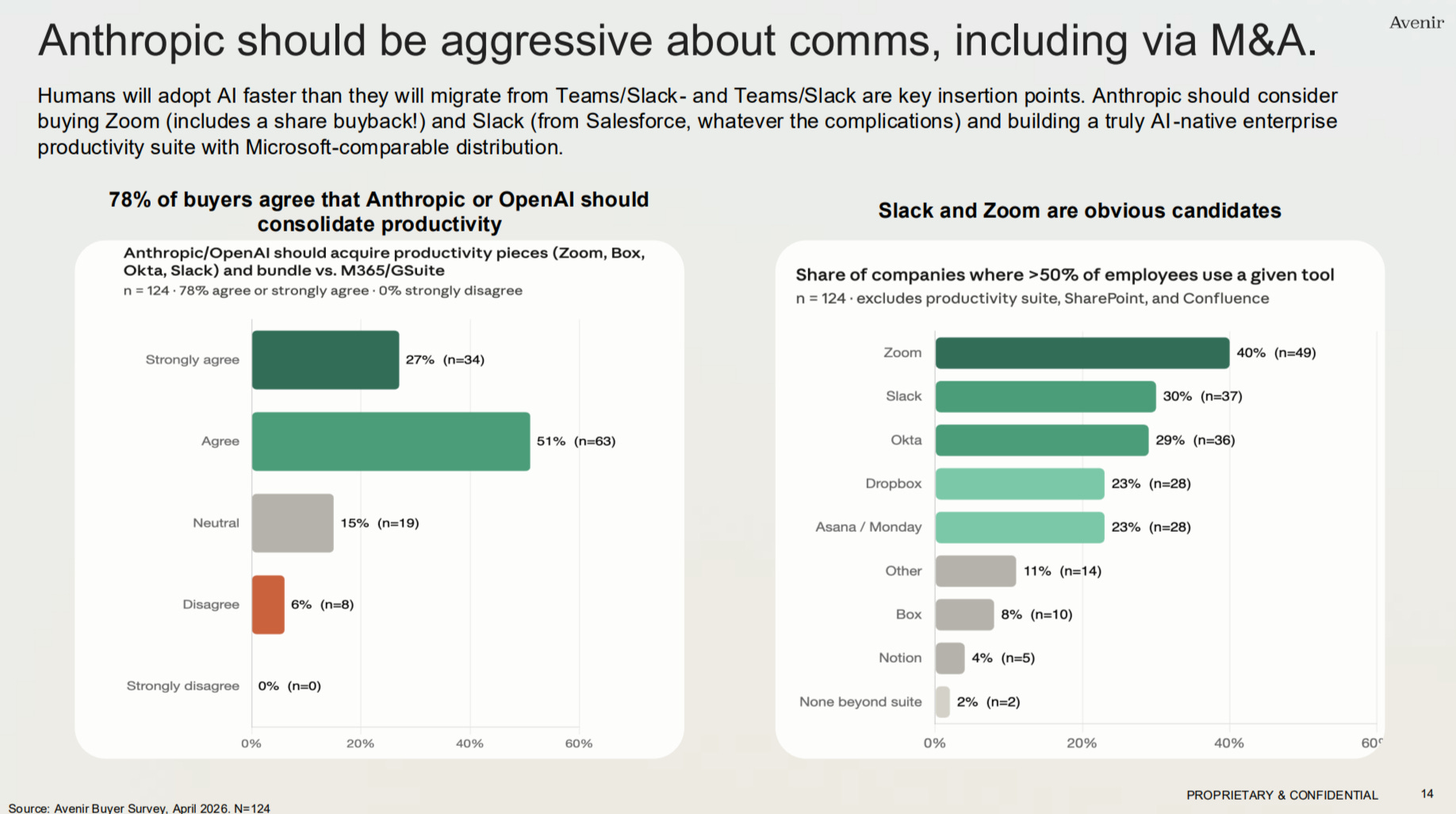

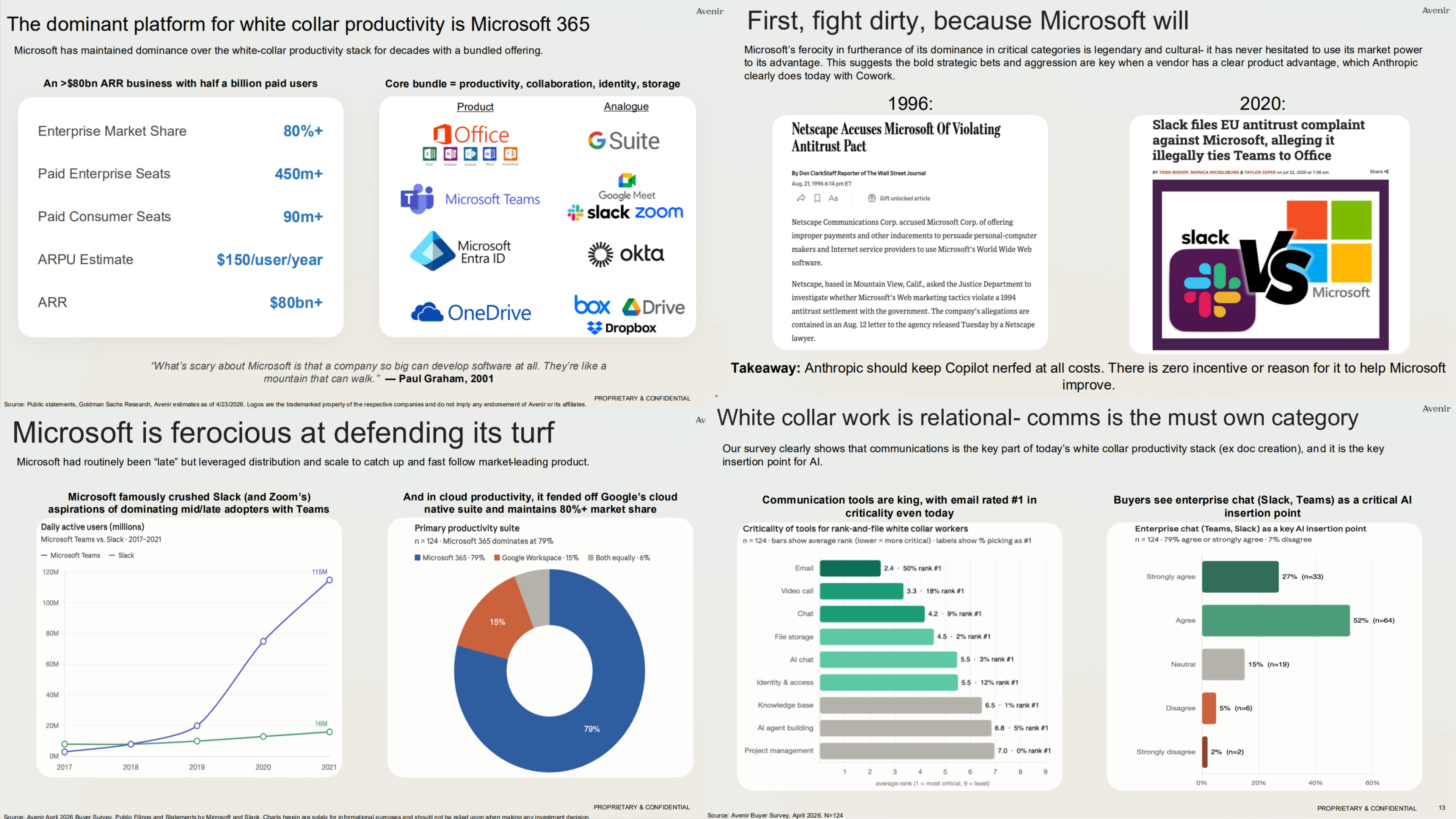

Jared Sleeper from Avenir published “How to Distribution-Mog Microsoft: Anthropic’s Path to Building the White Collar AI Platform” (16 slides). Our excerpts focus on their primary survey work, showing an interest in a) paying a premium for better AI and b) customers wanting M&A (as our research has shown, software buyers prefer platforms over point solutions, even when “best of breed”):

This 4-in-1 excerpt gives a sense of the strategic angles in the deck:

While focused on Microsoft, this thesis left a:

stronger appreciation for the Google moat (specifically, Workspace + Gemini + Google Cloud, both in terms of compute + custom enterprise applications to the extent enterprises are also on platforms like BigQuery) in an AI world where “mogging” Microsoft has become a point of debate.

The customer demand/interest in comms M&A is intriguing from a first principles perspective: Why would Anthropic owning Zoom or Box/Dropbox really change things? (Monday/Asana makes a bit more sense). What does this mean for feature gaps in AI <> SaaS integrations? Just a function of not wanting to do yet another integration (again, buyers do perform platforms)?

Curated Content

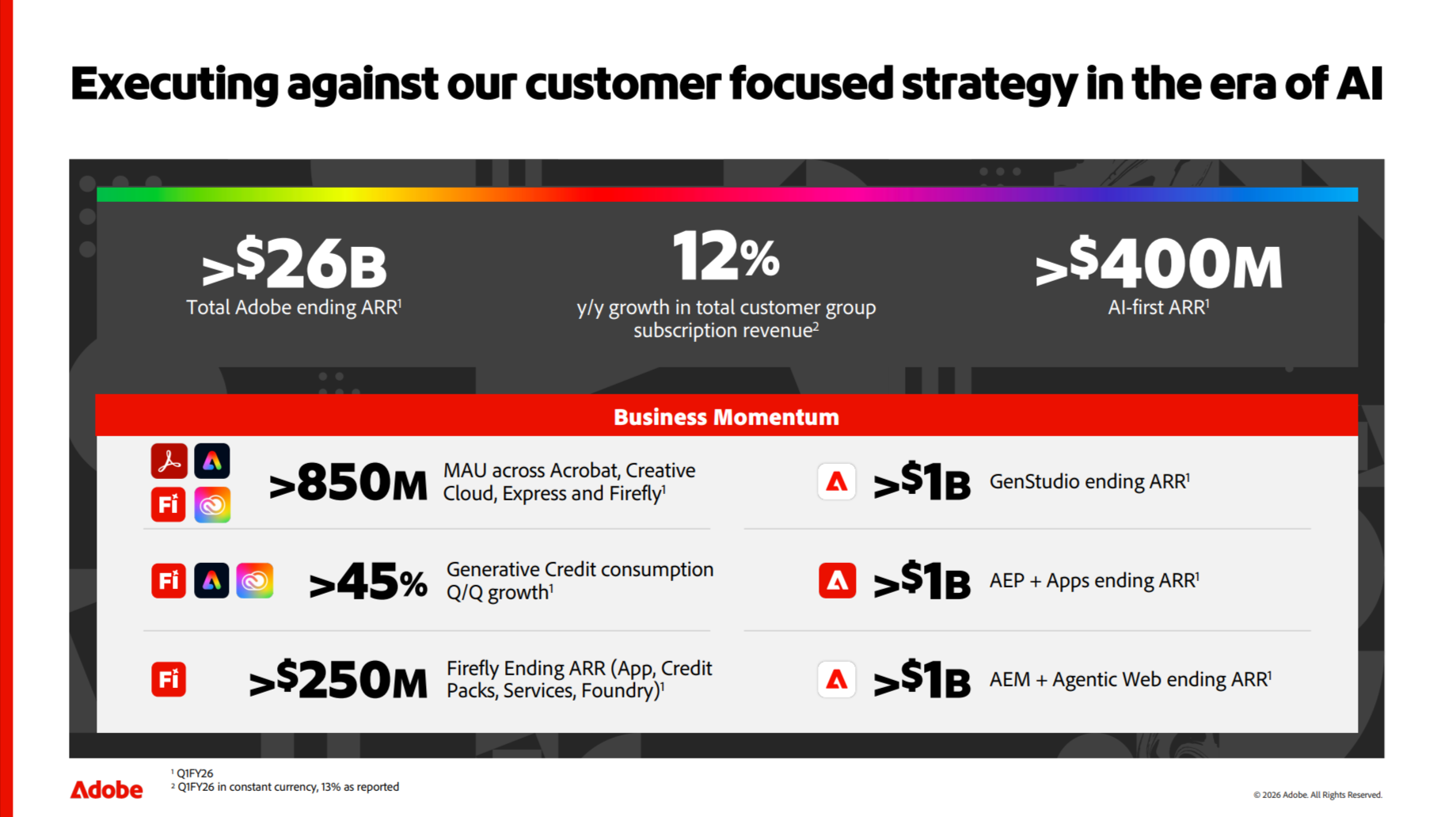

A status check on AI ramp at incumbents: Adobe disclosures from their Adobe Summit 2026 (n=1 here... but big!):

$400m "AI-first ARR" = 1.5% of total ARR

$1b "GenStudio ARR" = 3.8% of total ARR

Generative AI credits growing +45% quarter over quarter = 377% annualized (yes, that high given exponential in QoQ at 45%!)

Lazard’s “AI Impact on Technology M&A” deck (60 slides) mentioned above is worth a rehighlight - strong aggregation of AI frameworks + studies.

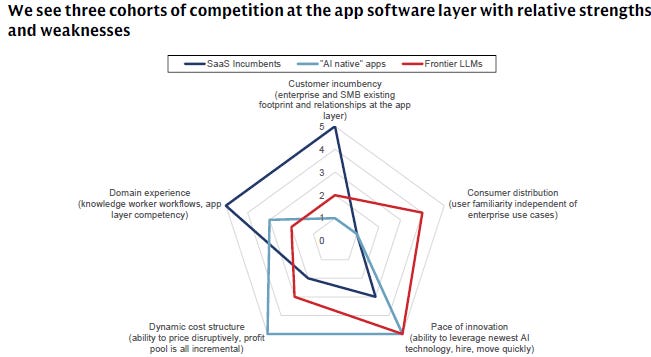

This competitive framework from Goldman Sachs was interesting. TBD on the weighting of consumer familiarity - equal weighting would require a substantial increase in the “consumerization of IT” within enterprises, more than realized in past cycles… that said, AI is truly an epoch shift.

About Cloud Ratings

In mid-2024, we announced a research partnership with G2 - more here:

with this slide showing how our G2-enhanced Quadrants (like our recent Sales Compensation Software) release, this business of software newsletter you are reading, our podcasts, and our True ROI practice area all fit within our modern analyst firm:

Best Substack yet. Great write-up Matt!