SaaSletter - Mixed Market Signals

Plus Our October 2024 SaaS Demand Index

High Alpha 2024 SaaS Benchmarks

Building on OpenView Ventures’ benchmark history, High Alpha released its 2024 SaaS Benchmarks report (n=800, mainly in the $0-$20m ARR range).

Our quantitative research at Cloud Ratings has identified very early-stage vendors - even sub $1m ARR - as a “canary in the coal mine” forward indicator for the broader sector. As such, this chart is somewhat bullish:

Given Zylo’s software spend under management ($30b plus), this preview of their 2025 SaaS Management Index was particularly notable for “enterprise +” (i.e. 2,500+ employees) showing double-digit growth:

Zylo Related Resources: I joined Ben Pippenger on their podcast to discuss their 2024 report and hosted Cory Wheeler on our podcast covering their 2023 report

That said, there are only slight (at best) signs of growth acceleration in the broad index captured by Paddle (“Paddle manages global payments complexity for SaaS and digital product companies, so you don’t have to.”) beyond this survey sample:

As always, go read the full report. While I focused on broad market indicators here, the report covers both core SaaS metrics (retention, growth, Rule of 40, ACV, headcount mix) and some novel areas like founder wellness and in-office vs remote growth rates:

Maxio Q3 2024 Data → More Mixed Signals

Maxio released its industry data through Q3 2024.

Like the High Alpha report, the sub-$1m revenue trendline is encouraging as a forward indicator. That said, the above $1m revenue growth rates are trending towards unacceptable relative to the software industry’s cost of capital.

The sharp deceleration in usage growth rates was also concerning.

There is a good bit more in the full report - like growth rates by end market → go read it.

October 2024 Demand Index

We’re excited to update the SaaS Demand Index with data through October 2024.

Due to an ongoing, partial shift in Google’s methodology, this month’s sample consists of 71 companies (versus our usual 340) covering 100,000+ high-intent searches. However, all graphs and metrics are pro forma on a historical basis (i.e., apples to apples).

Reminder: this is a directional, free, and ever-evolving analysis → always do your own due diligence. Moreover, the data captured here is best characterized as top-of-funnel or dark funnel → factoring in sales cycle length, do NOT use this Demand Index as a predictor of near-term financial results and/or financial guidance.

High-intent search volumes were up +4.6% year-over-year but down 5.9% month-over-month. Given ongoing Google methodology changes, consider this reading highly provisional.

Of note, across many ~#altdata indicators that we track (but do not publish), we see a) heightened volatility and b) a widening gap between the top 10% / top 25% and the rest of the software.

Curated Content

My vote for the best coverage of the ServiceTitan IPO filing = Meritech’s write-up

The Deal Director on a surprisingly undercovered topic: “The partner dilemma in tech sales revisited”

Dave Kellogg on “The Proper Role of the Board Observer”

Google Cloud and DORA released their “2024 Accelerate State of DevOps Report” - with my excerpts + ChatGPT’s “7 out of 10” opinion of the DevOps AI read through here.

Rob Litterst and PricingSaaS.com released their Q4 2024 SaaS Pricing Benchmarks

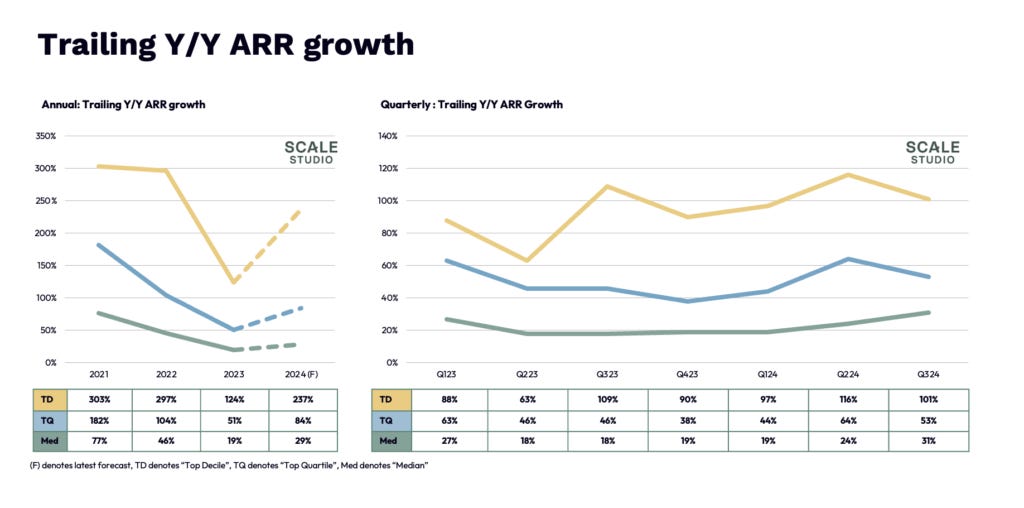

… and one last market indicator - Scale Venture Partners Q3 2024 Flash Report:

About Cloud Ratings

In case you missed it, we recently announced a research partnership with G2 - more here:

with this slide showing how our G2-enhanced Quadrants, this newsletter, our podcasts, and our growing True ROI practice area (see Ivan Arizaga’s appointment as a Principal Analyst) all fit within our modern analyst firm:

It’s fascinating how early-stage SaaS signals agility and innovation, yet scaling exposes cracks in larger players. Zylo’s enterprise growth feels like a spotlight on untapped efficiency goldmines.