SaaSletter - ICONIQ's "State of AI"

Plus Cloud Ratings B2B AI Interest Index for December 2025

ICONIQ’s “State of AI: Bi-Annual Snapshot”

ICONIQ (h/t Vivian Guo and team) recently released its “State of AI: Bi-Annual Snapshot” report (44 slides, ungated).

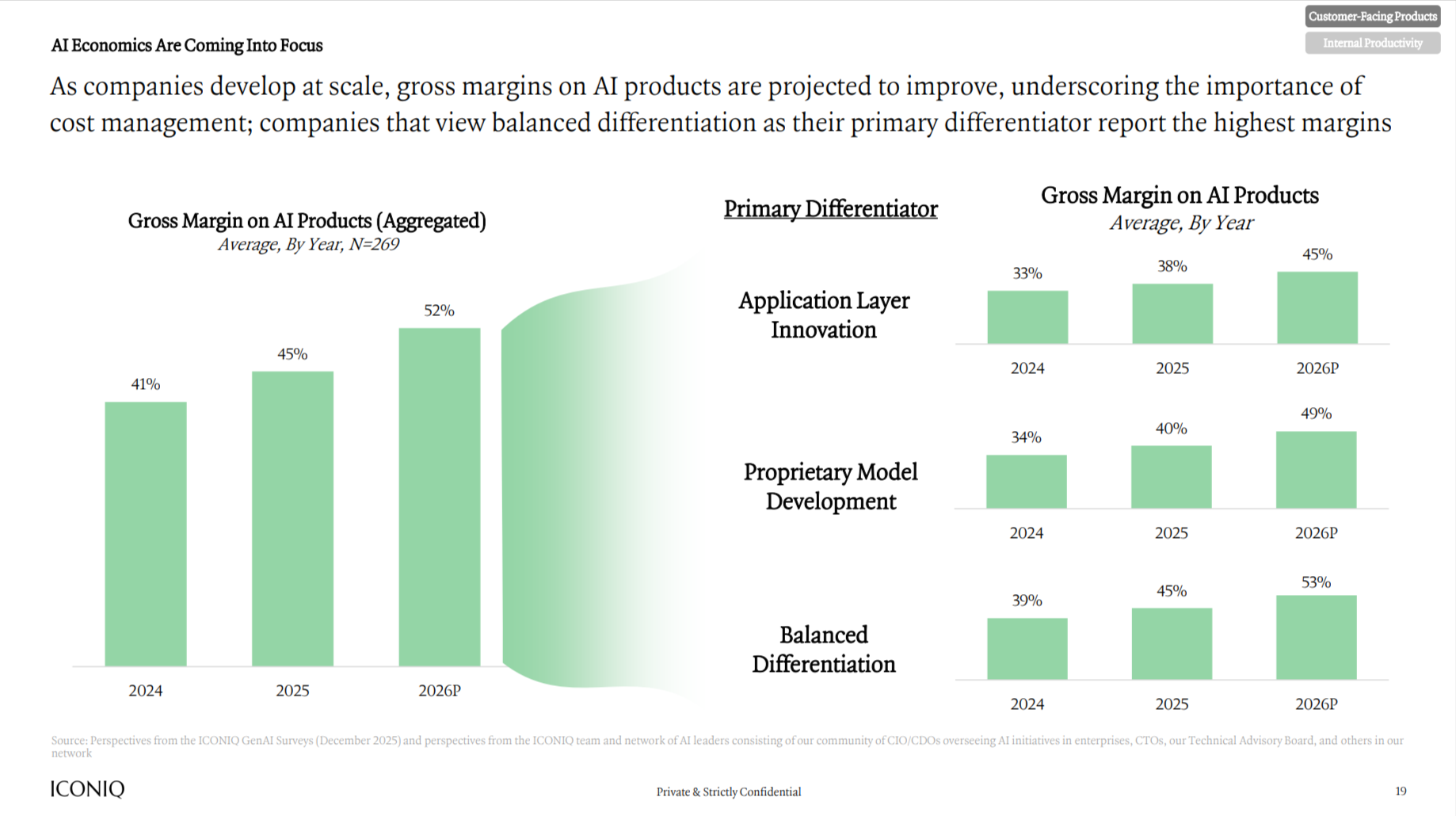

Key call-outs: while AI product gross margins are projected to increase by ~700 bps (‘25: 45% → ‘26e: 52%):

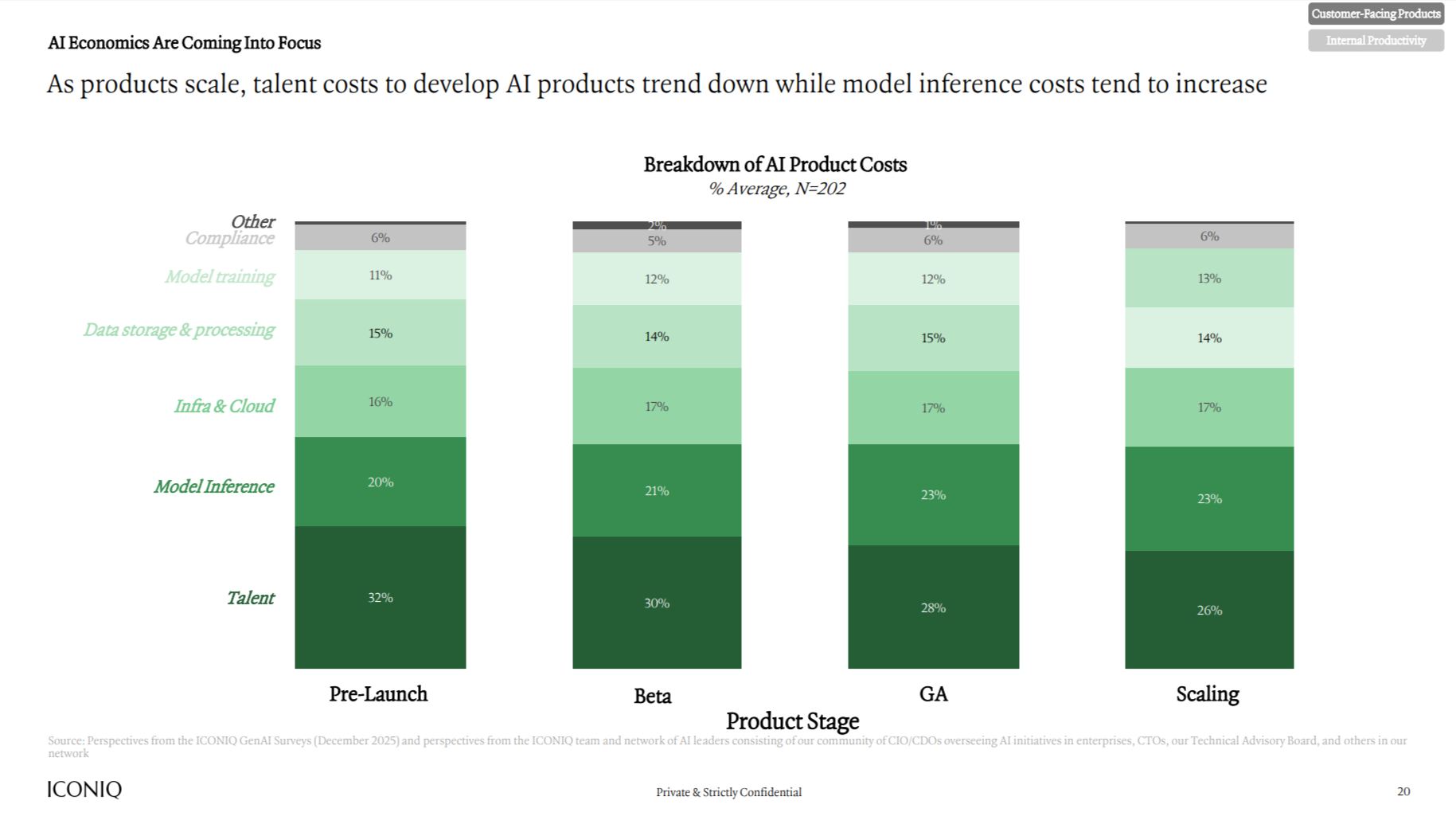

… the fabulously granular cost structure breakdown makes those margin increases look optimistic. “Talent” - a largely fixed cost - is only 26%-28% of the cost structure for the GA to Scaling stages. All other costs are highly variable, such as inference and cloud costs. Even for model training, there is little fixed cost leverage since model training is an ongoing process. Key message: There seem to be too few fixed costs to generate software economics.

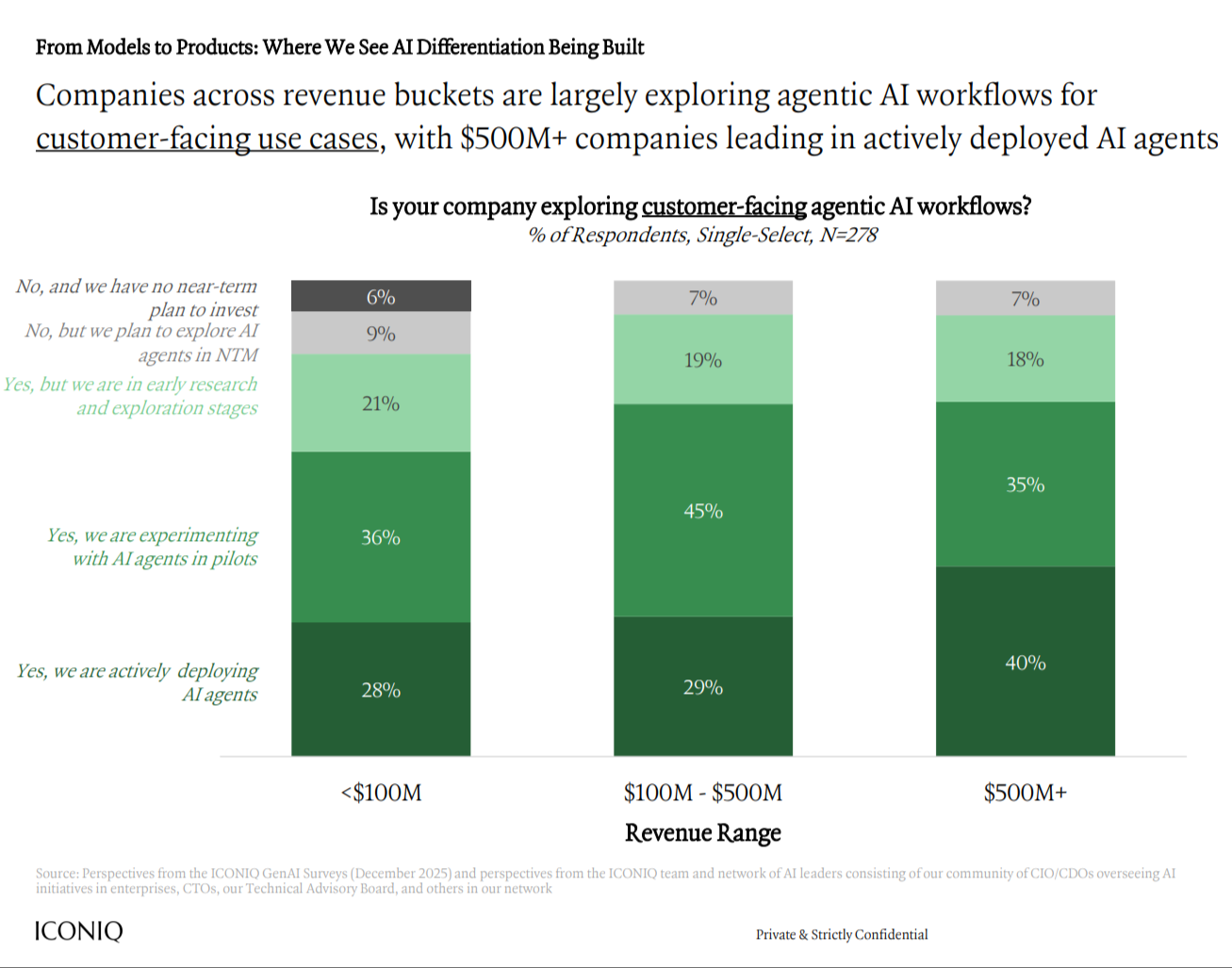

Notably, larger organizations (>$500m revenue) are the leading deployers of customer-facing agentic AI.

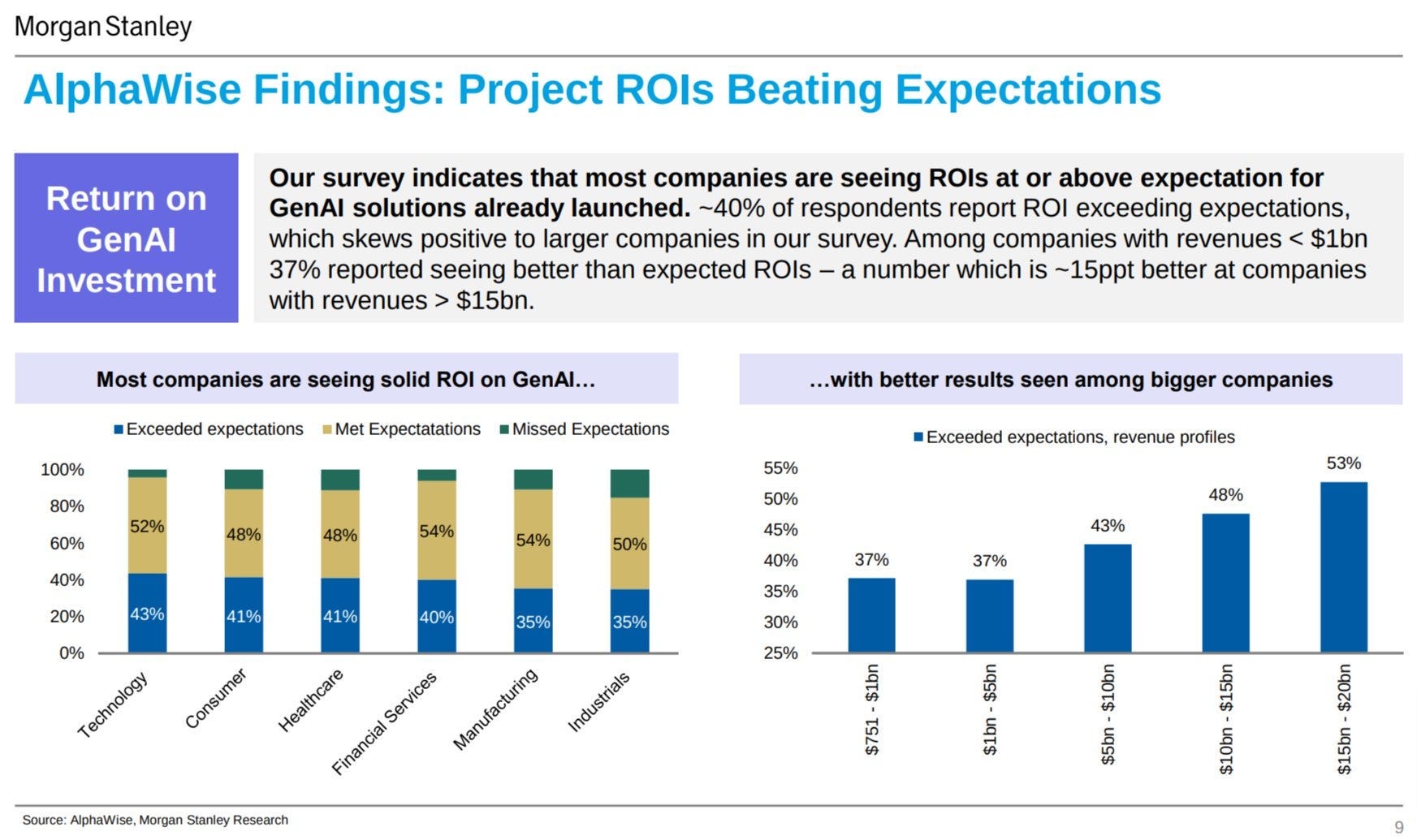

The increasing AI deployment and returns to scale are consistent with our 2023 formula below (with emphasis on the volume variable) and Morgan Stanley findings that large enterprises are achieving the highest ROIs:

AI ROI = (Business Process Value x Volume) / AI Costs

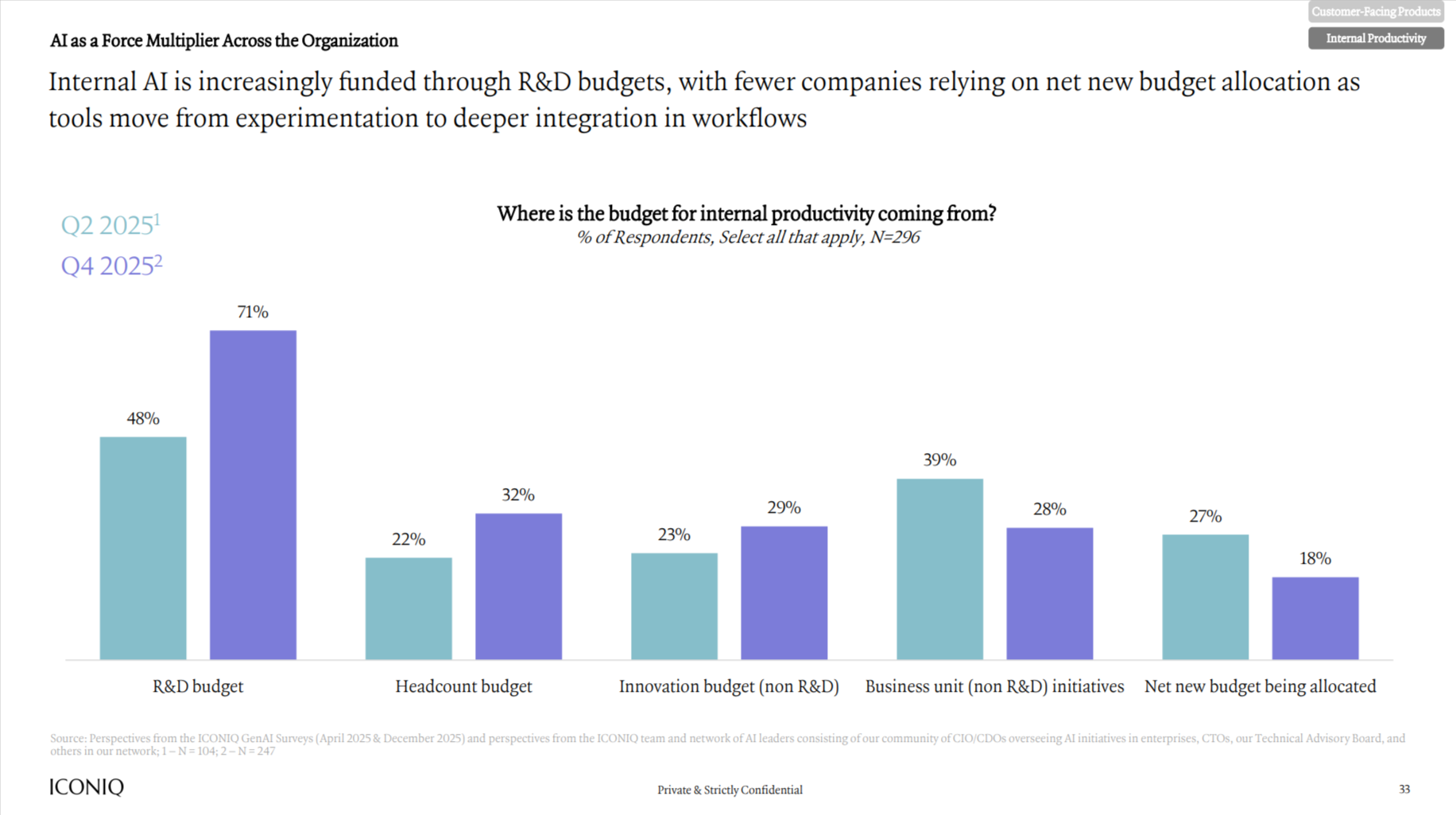

Back to ICONIQ, flagging this data + commentary as a headwind: “Internal AI is increasingly funded through R&D budgets, with fewer companies relying on net new budget allocation.” This could have implications for both AI vendors (i.e., hitting budgetary guardrails + enterprise reality checks) and non-AI software vendors (i.e., AI truly competing in the same IT dollar pool rather than a separate “innovation” budget).

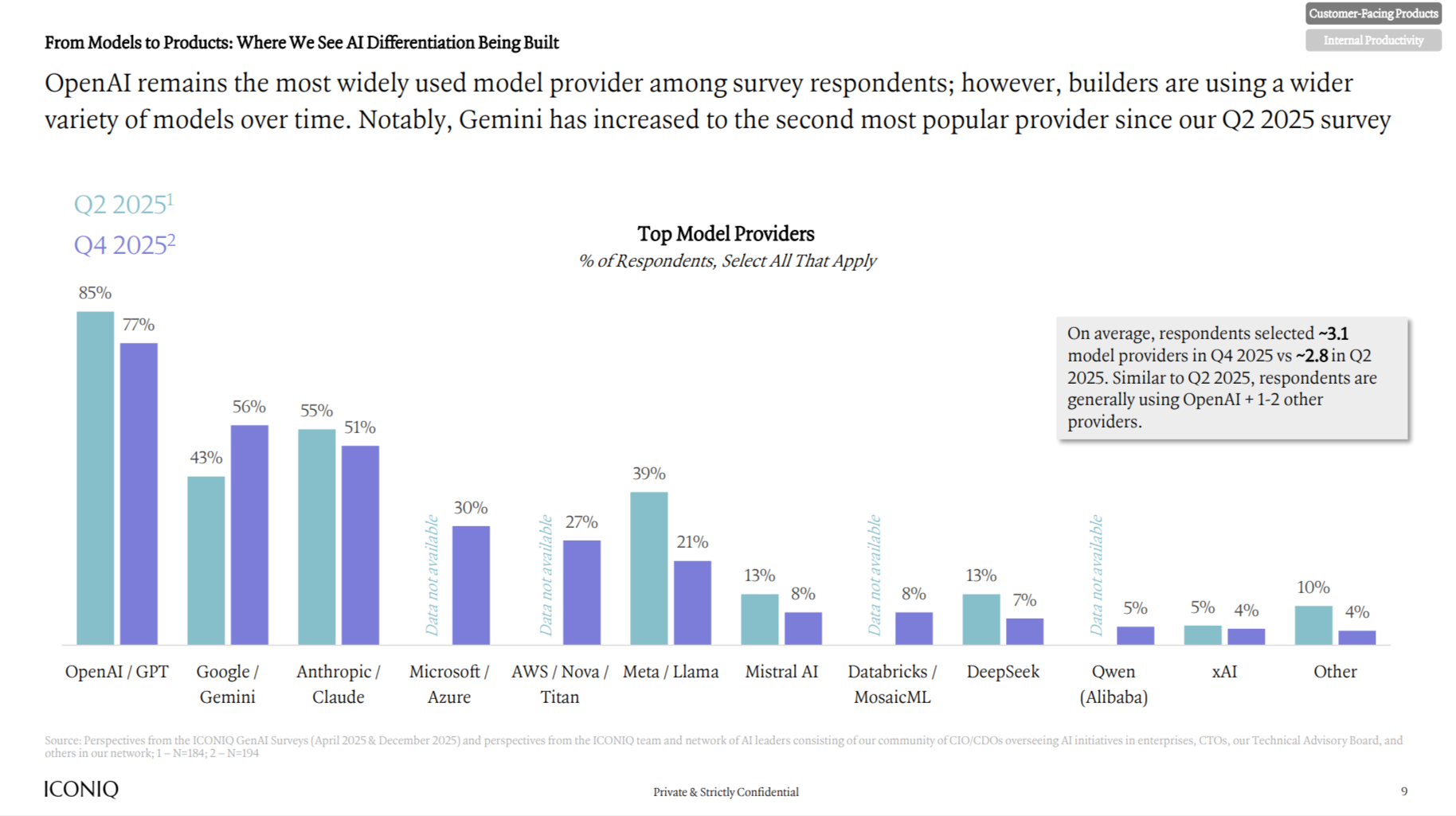

If you know, you know (“IYKYK”), any and all AI model market share charts attract a lot of “attention” amongst VCs:

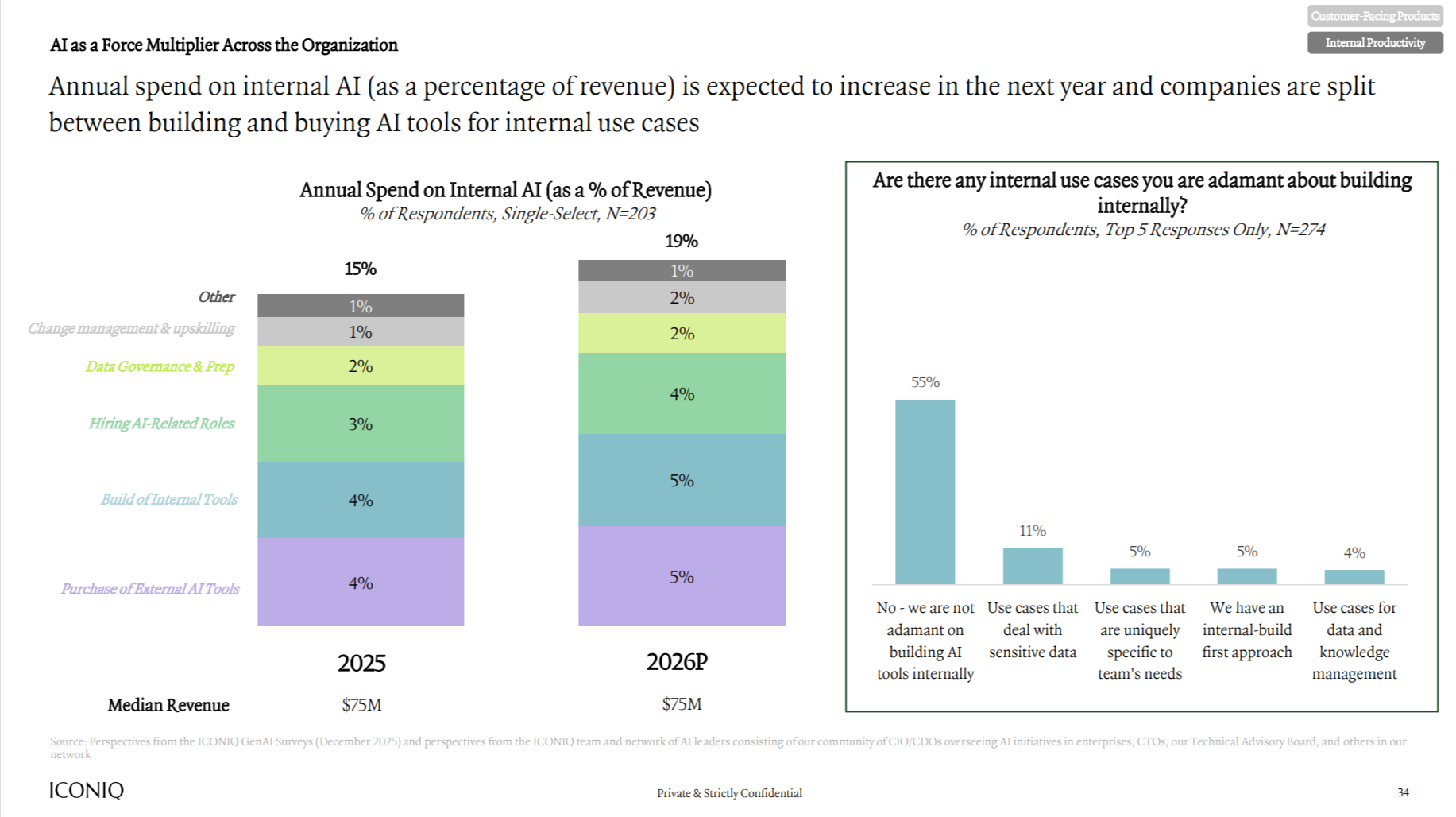

And yet another data point for the “buy versus build” component of the “Software Is Dead” daily debate:

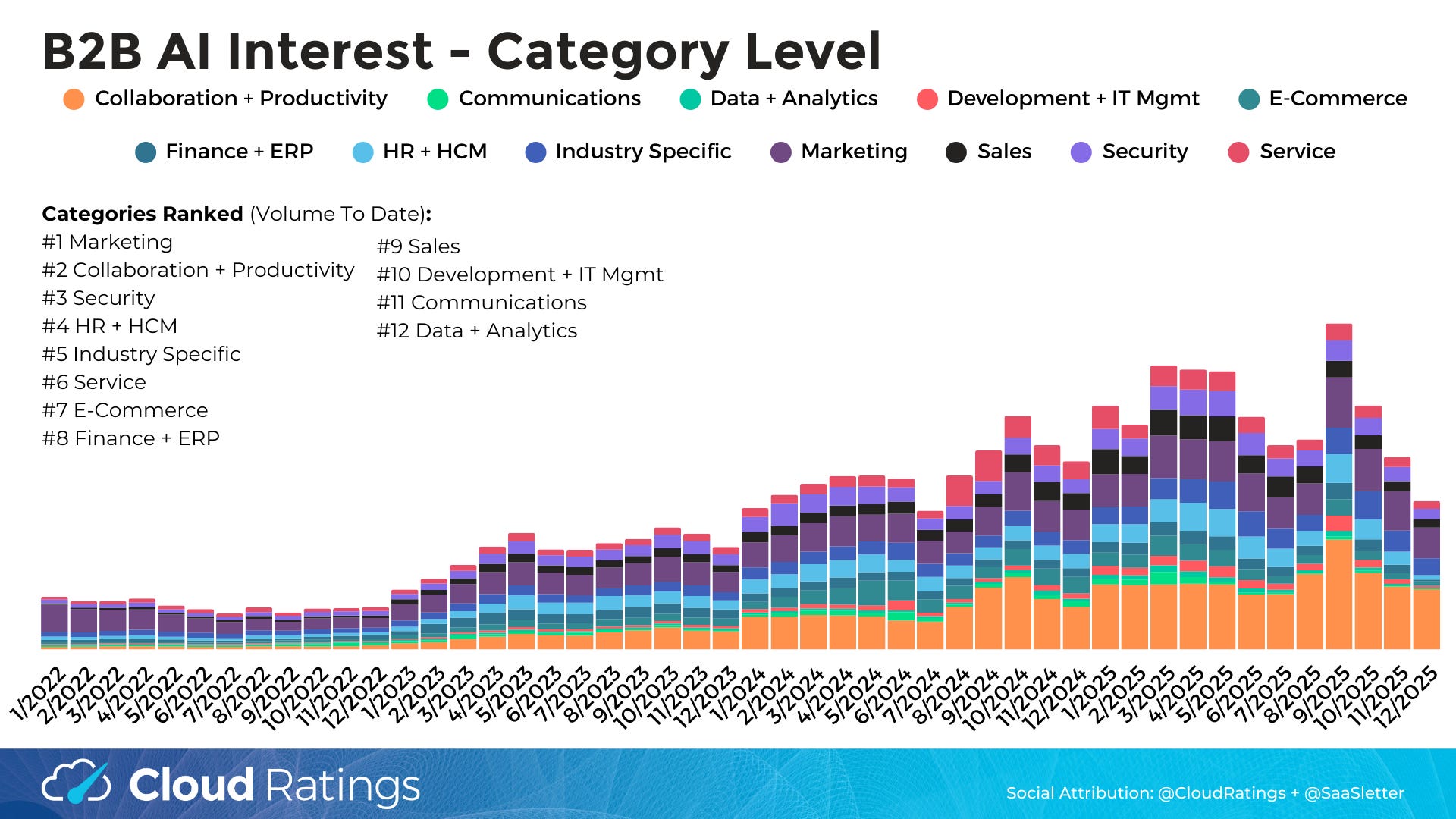

December 2025 B2B AI Interest Index from Cloud Ratings

We’ve updated our Cloud Ratings B2B AI Interest Index through December 2025 - full slides below:

Thematic Category Interest (n = 47 sub-categories tracked - i.e. “manufacturing AI” or “supply chain AI”) registered a notable decline. Note: holiday seasonality will be at play throughout this month’s report. Beyond seasonality, as AI-native vendor brands strengthen, generalized product searches might be losing share to brand-targeted search.

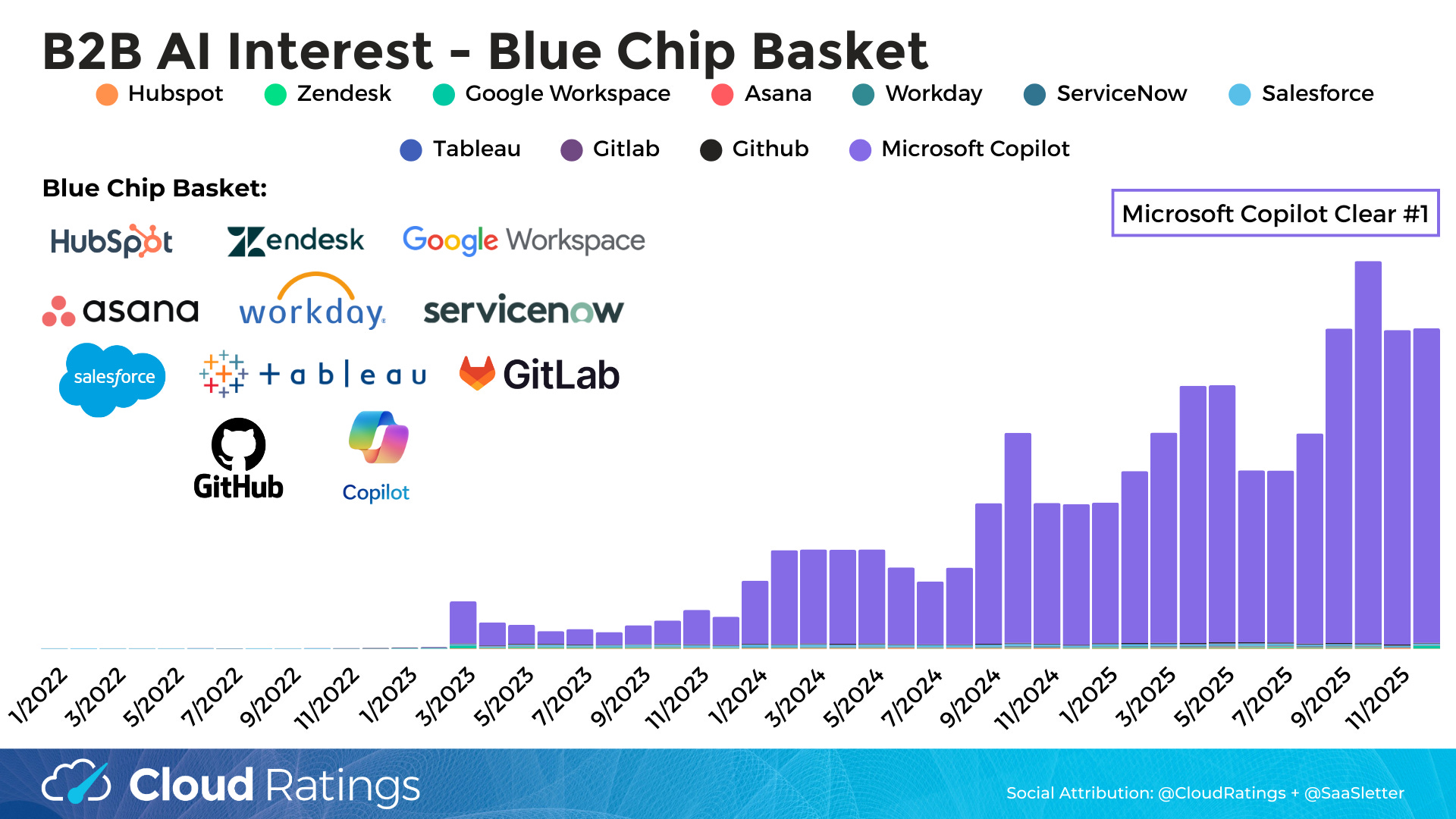

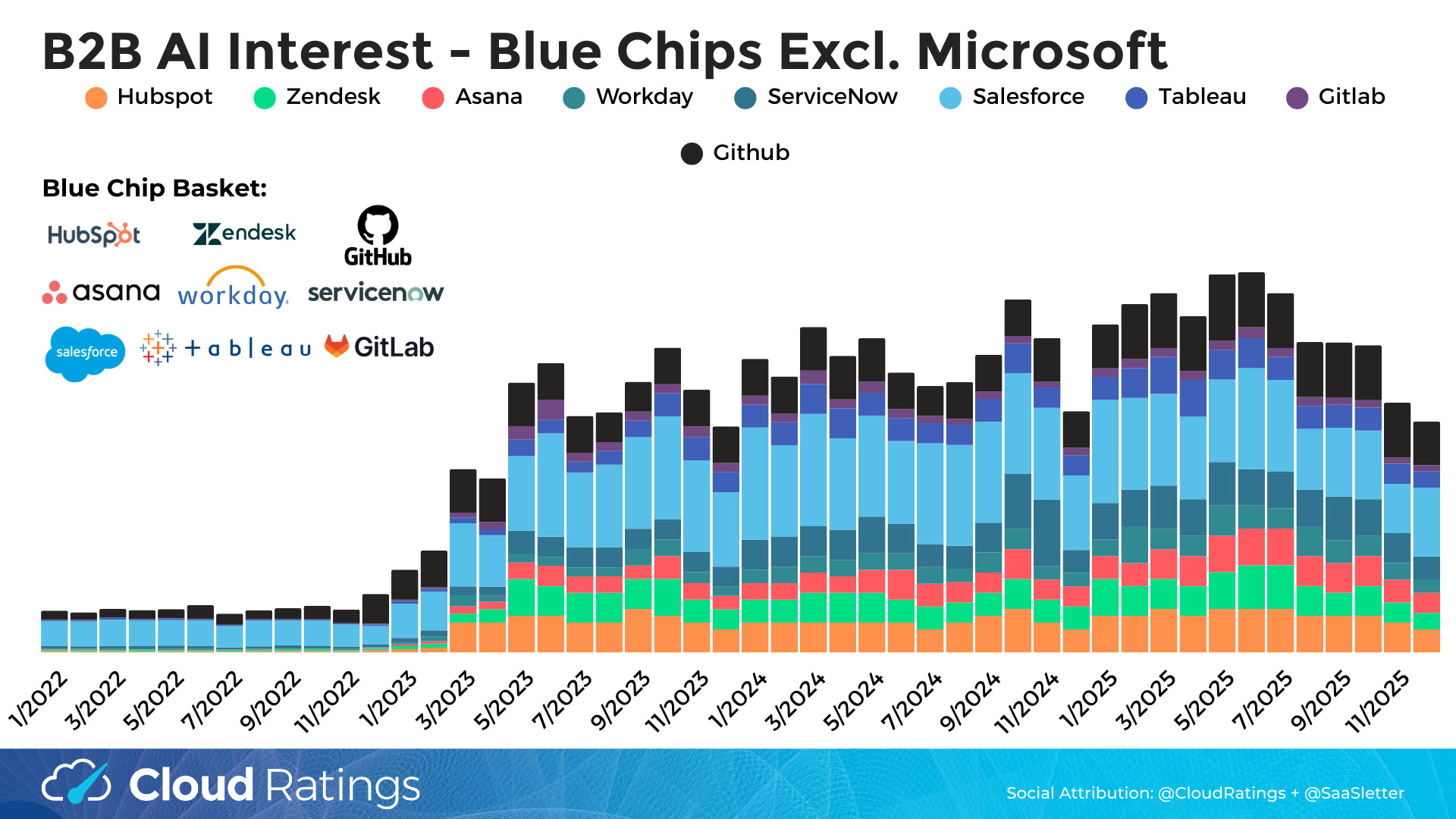

Bellwether Microsoft Copilot continues to stay at a higher plateau. Other “Blue Chips” (i.e., Hubspot, ServiceNow) had a weak December (down 4% YoY, so not just seasonality here).

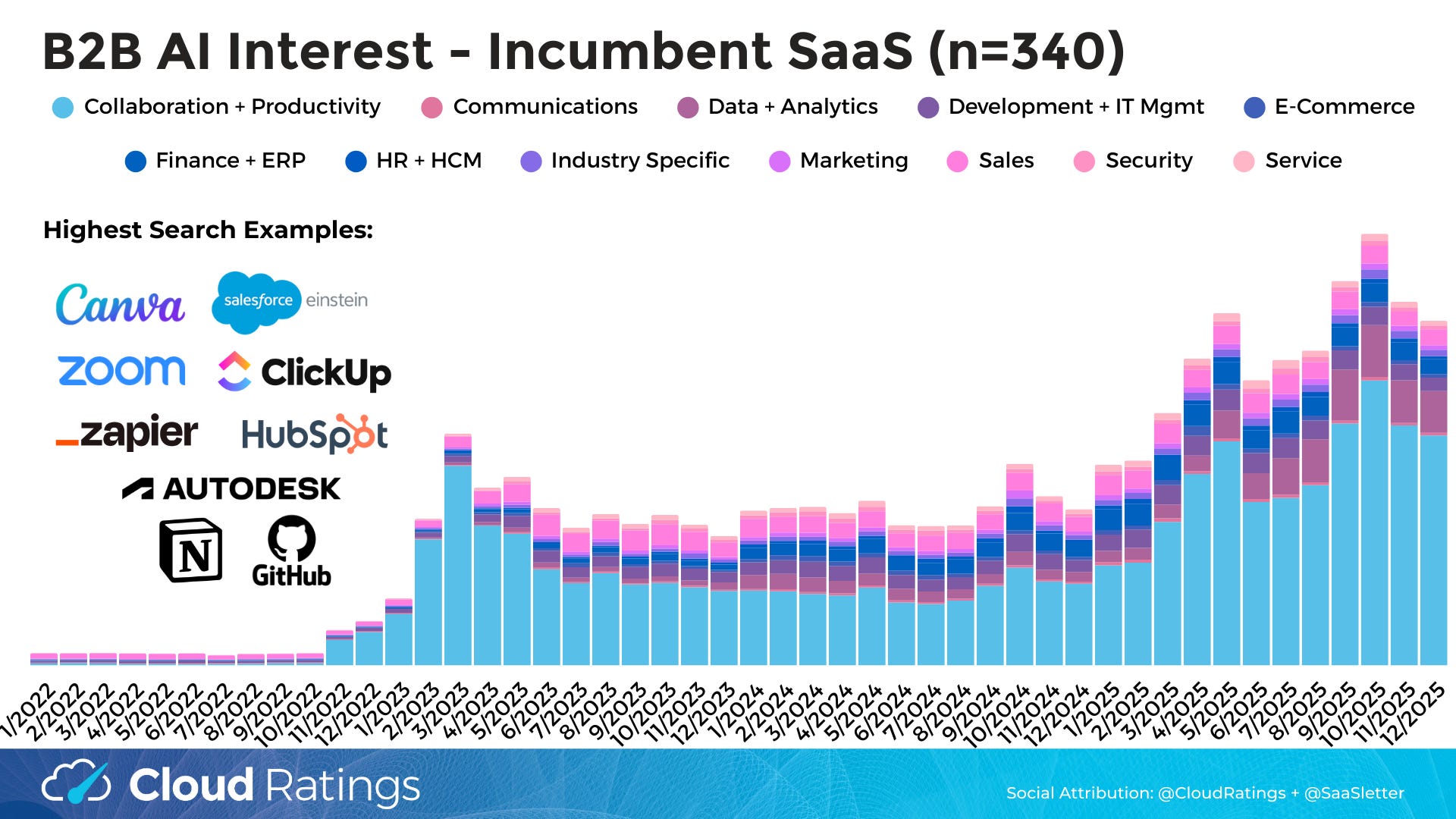

SaaS Incumbents (n=340: the same 340 vendors tracked in our top-of-the-funnel focused, forward-looking SaaS Demand Index) registered a seasonal MoM dip, but interest in the Incumbent basket is up 119% YoY.

About Cloud Ratings

In mid-2024, we announced a research partnership with G2 - more here:

with this slide showing how our G2-enhanced Quadrants (like our recent Sales Compensation Software) release, this business of software newsletter you are reading, our podcasts, and our True ROI practice area all fit within our modern analyst firm: