SaaSletter - All AI: Buck, Sequoia, Barclays, McKinsey, + More

Plus Cloud Ratings new May 2024 B2B AI Interest Index

Buck on AI x Software

Buck on Software published a very thoughtful “Winds of Change” post. I’ve heavily excerpted here with all bolding added by me:

The river of AI is likely to flow around the massive existing rock formation that is deterministic software. Gradually eroding it away versus sweeping it away. Software bears are leaping to a fully eroded end state (fully autonomous agents). But that end state is likely well over a decade away.

In the interim period, most existing software vendors have a right to win and to gradually rebuild themselves from workflow wrapped around a database, to workflow with some AI infused wrapped around a database, to workflow and AI agents wrapped around a database, to AI agents wrapped around a database. This is going to happen iteratively with heavy involvement of human end users who today work within existing systems. This gives incumbents an advantage, if they act aggressively to use it.

Some additions to the above from Buck:

Jared Sleeper: his new enterprise IT buyer survey showed 68% stating, “Our existing software vendors will generally be beneficiaries of generative AI,” 27% neutral to incumbents, and only 5% seeing incumbents losers from AI.

Me: re: AI-enhanced SaaS will “happen iteratively with heavy involvement of human end users” → the a) non-deterministic nature of AI, b) related degree of *user* R&D (higher versus traditional SaaS), and c) challenges of QA’ing the last 1%-5%-10% of the workflow will represent a real switching cost + moat for any early AI winners, incumbent or AI-natives.

Now, back to Buck:

The Task TAM vs Software TAM:

What about seats? How will they price? I don’t think that matters much if this is a transition versus a major discontinuity. Historically, value in software has been easy to capture if created via a differentiated offering. And if software vendors are successful in the above outlined transition the “task TAM” is likely an order of magnitude larger than the existing software TAM.

Take Sales Cloud from Salesforce as an example. It is an ~$8B annual business today. It serves ~10 million users. Those users are likely paid $2-3 trillion in wages and benefits. It isn’t unreasonable to expect AI to automate 15% of tasks from this base of users ($300B) of which 10% ($30B) is captured by the vendor driving that increase

My addition to Buck above: re: his 10% value capture assumption →our meta-analysis of analyst ROI studies shows vendors capturing 36% of value creation (278% average 3-year ROI).

In some end markets, the size of the task TAM is unbounded, meaning that a substantial increase in low-cost human hour equivalents would drive a corresponding increase in business value. For example, software development has an unbounded task TAM. There is value to a business in creating a lot more software, assuming it is useful software.

This isn’t true for every end market of course. Increasing the number of tasks in the financial close process would likely not create much business value.

No additions to the above - all great points

Velocity is an Important Input

I think about the software market in two broad buckets. The first is low velocity categories where not much will change. For example, payroll processing is not likely to be impacted much by AI. …

The second bucket is where there is likely to be a lot of change. Creative, sales, marketing, customer support, workflow automation, RPA and software development are examples of these markets. The task TAM is large and in some cases unbounded. And while there is risk associated with change, there is more upside. This will create substantially more category velocity and many more new entrants. There is also significant TAM expansion that is likely to occur. The existing competitive advantages of vendors provide them a right to win, but they must act on it and invest heavily in AI first capabilities.

All of the above is consistent with my own view on AI (see my “State of the Industry” slides at Bowery Capital’s AGM) = by moving from “framing the work” (i.e. Jira) to “doing the work” (i.e GitHub CoPilot) which will have strong ROIs (very hard to compete with automation), AI will add an important second leg to the growth story of a maturing software industry.

Go read Buck’s full “Winds of Change” post.

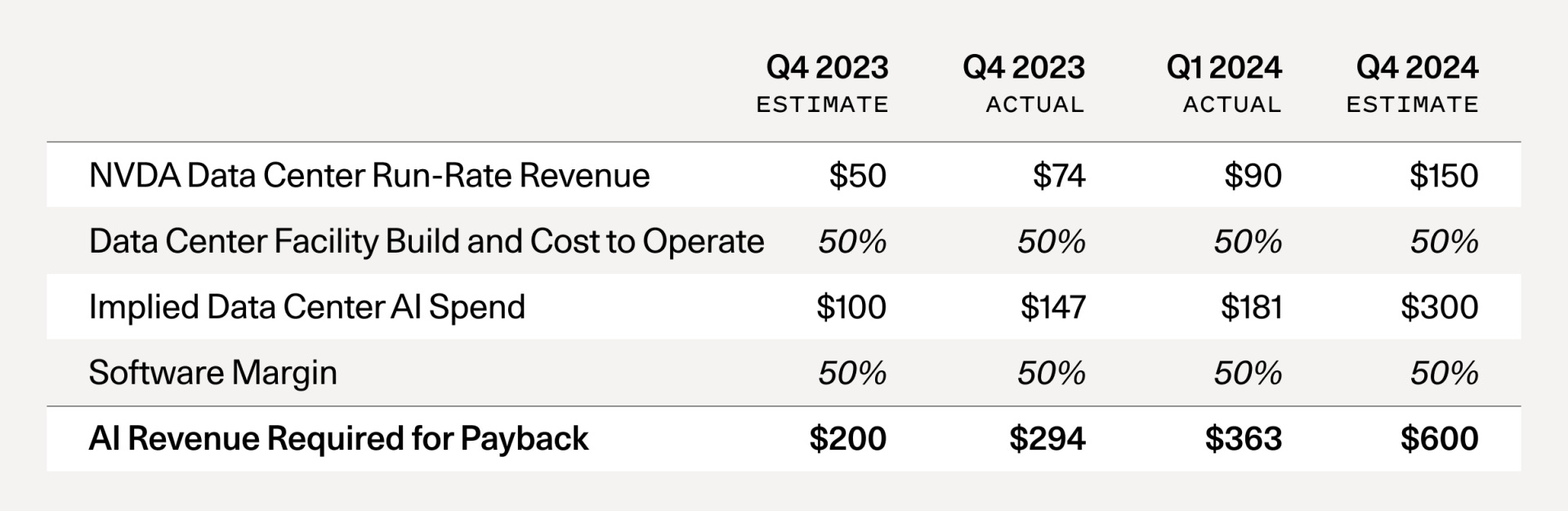

Sequoia’s AI Math Updated…

“AI’s $600B Question” - David Cahn from Sequoia updated his formula (table above) that addresses the “gap between the revenue expectations implied by the AI infrastructure build-out, and actual revenue growth in the AI ecosystem, which is also a proxy for end-user value.”

… and Barclay’s AI CapEx ROI Math

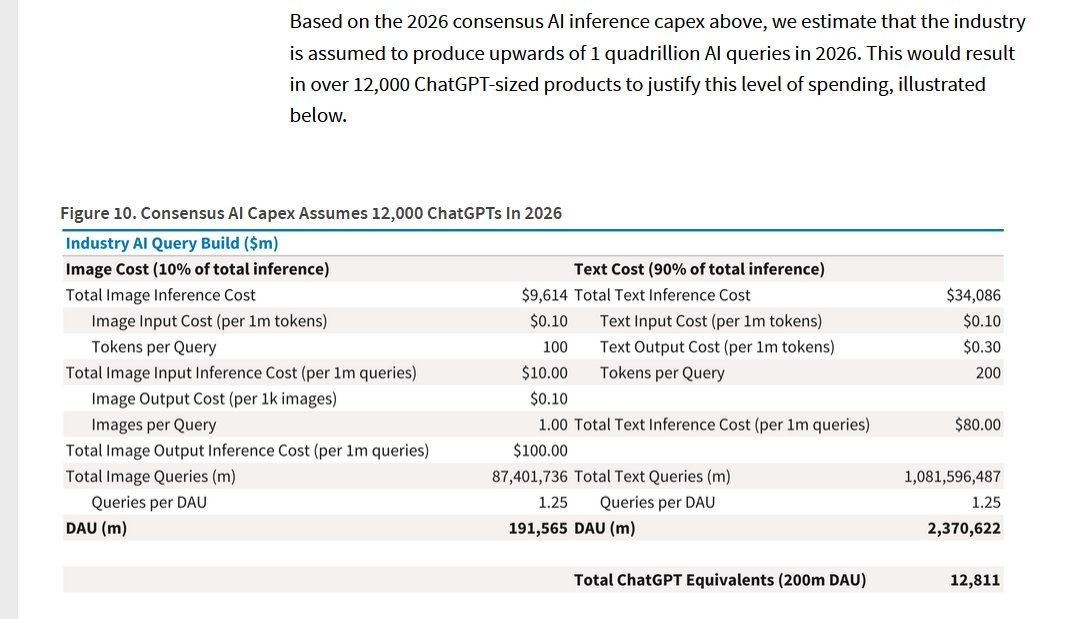

Meanwhile, Barclays published its own take on AI CapEx ROI - bolding = mine:

The basic math exercise starts by figuring out how much the big hyperscalers are spending in incremental compute-only capex from 2023-2026 (what we label as “cumulative AI Capex”), and then figuring out how much this capex can support in terms of new AI products for consumers and enterprises. The quick conclusion – we are more in the FOMO camp, as the street is modeling $167B in cumulative AI capex from the top players in the industry, which, as noted above, is enough to support over 12,000 ChatGPTs. We estimate that around $70B will be invested in training foundation models, leaving roughly $95B for inference (i.e. “the cost of serving up finished products”).

We think one of the big players may blink and cut back the capex plans, but not likely until we get well into 2025 or beyond.

We’d also note that recent breakthroughs in the smaller foundation model space are likely to bring a ton of products and queries away from the cloud and towards the edge (i.e. – running natively on a PC or a phone) by 2026, which may further pressure the need for this large level of AI capacity in the cloud.

Barclays also framed the implied AI query volumes relative to existing web search:

Based on these estimates, Google is assuming around 180T AI text queries (both input and output) and 15T AI image queries. This is a staggering figure, as there are around 11T web search queries per year right now worldwide. Stated differently, Google’s AI capex assumes a market that is 15x-20x larger than the web search market by 2026.

McKinsey’s Latest on AI x Software

“Navigating the generative AI disruption in software” - by Jeremy Schneider, Tejas Shah, and Joshan Cherian Abraham

My quick excerpts and annotations. This chart speaks for itself: AI on track for 3x penetration versus the historical SaaS adoption curve:

You could interpret this chart in two ways:

1 - AI increases software vendor “switching” (~gross churn) by 75%! 2 - AI “only” takes vendor switching

or 2 - AI “only” causes a moderate amount of vendor switching in absolute percentage terms, seemingly consistent with Buck’s “Winds of Change” takes

Interesting data here, especially 2027e $175b-$250b enterprise spending on GenAI:

This category exhibit is worth consuming with Buck’s “low velocity vs high velocity” framework in mind:

There is a good bit more in the McKinsey June 2024 AI report, which you should read here.

Curated AI Content

“BVP State Of The Cloud 2024” - in terms of AI, I found the 65% gross margins notable. See my earlier coverage of gross margins in “Coatue on AI -> SaaS Read Throughs”

AI investors Nathan Benaich + Alex Chalmers from Air Street Capital have had a good, sober series of essays:

“Alchemy doesn’t scale: the economics of general intelligence”

“Alchemy is all you need: On the economics of frontier models”

KKR’s “Mid Year 2024 Outlook” macro report was bullish on AI driving greater economy-wide productivity growth similar to the 1990s Internet boom:

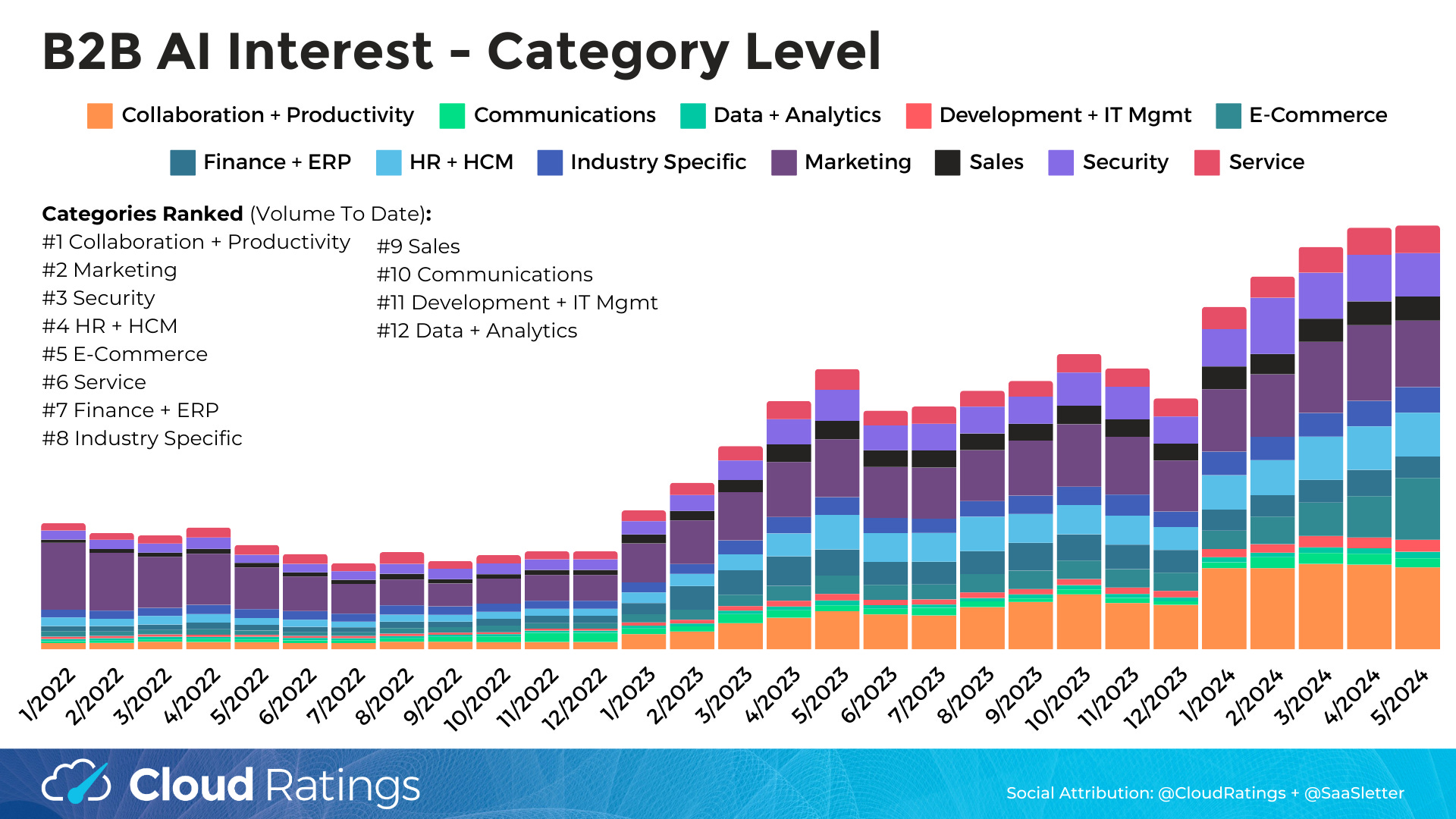

May 2024 B2B AI Interest Index from Cloud Ratings

We’ve updated our B2B AI Interest Index through May 2024 - full slides below:

We’ve organized the slide highlights below from most favorable to least favorable.

Once again, encouraging trends at the thematic Category Interest (i.e. “manufacturing AI” or “security AI”) level:

Again, flat month-over-month interest levels for bellwether Microsoft Copilot, with other “Blue Chips” staying within a capped range:

A tiny increase for SaaS Incumbents (n=340, same 340 vendors tracked in our SaaS Demand Index):

Interest in AI Natives (n=50) *declined*:

Bonus: Maybe Accenture AI Bookings + GS/Gartner Math Helps?

Accenture recently reported quarterly AI bookings of $900m (or $3.6b annualized).

When combined with these estimates + timelines from Goldman Sachs and Gartner:

Assuming Accenture’s AI bookings are largely for “AI Prototypes,” the chart implies :

Data Modernization (~2026-27): $3.6b x 15 = $54b additional AI project spend for Accenture clients alone

AI Transformation (~2028-2031): $3.6b x 150 = $540b additional AI project spend from Accenture clients alone

→ Beyond Accenture Gross-Up: Making the (risky?) assumption Perplexity calculated this correctly, Accenture represents 1.3% of global IT services spend, so we need to 77x the ($540b + $54b above estimates) to arrive at cumulative IT service-vendor-managed AI spend of *$46 trillion* through 2031. With these dollars largely kicking in starting in *2029*.

Versus Accenture (ACN) Consensus: ACN’s cumulative forecasted revenue through 2031 is $667b. This means *our* mechanical application of the GS/Gartner chart would imply AI represents 89% of Accenture revenue. Hmmm? Or Wall Street consensus is underestimating AI upside (surely, non-AI “blocking + tackling” IT work will continue to generate billions for ACN)?

Many, many caveats apply here. Do your own work. This *free* newsletter is not investment advice regarding Accenture or anything else.

About Cloud Ratings

In case you missed it, we recently announced a research partnership with G2 - more here:

with this slide showing how our G2-enhanced Quadrants, this newsletter, our podcasts, and our True ROI practice area all fit within our modern analyst firm: